Hello and welcome to a new week - hope you have a good one!

The latest Global Cross Asset Market Monitor [Market Chart Pack] is attached below:

Topdown Charts Global Cross Asset Market Monitor 12012026

Global Markets Monitor -- Notable Developments

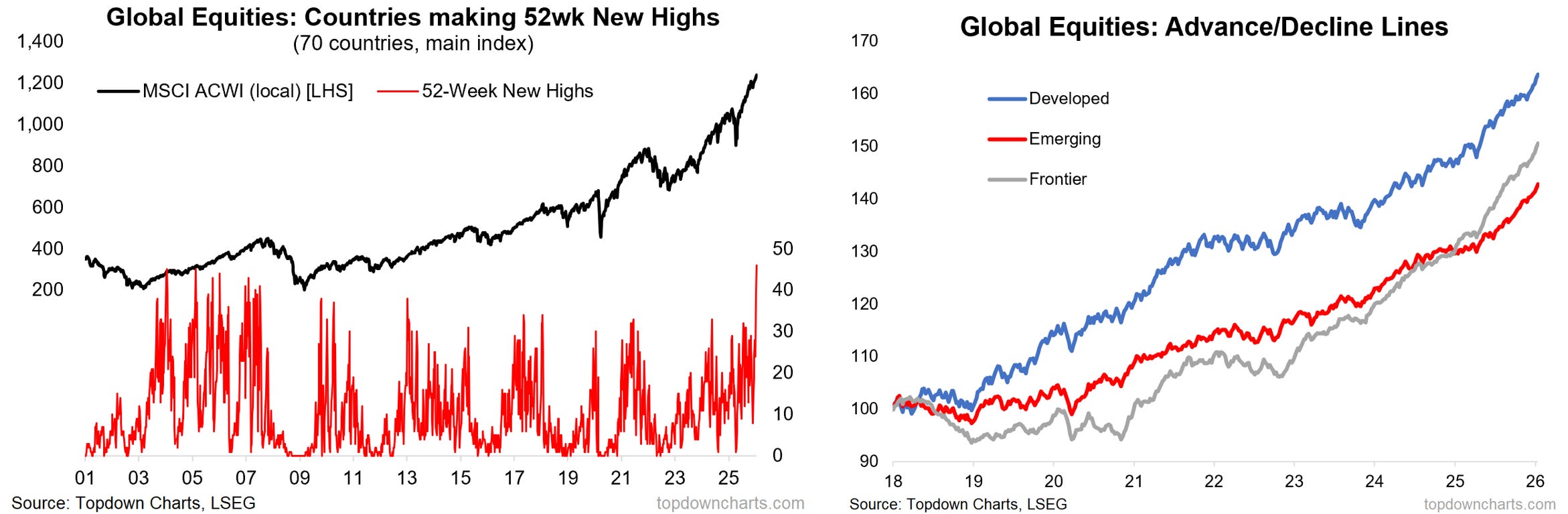

Most equity markets moved higher last week, most notably we’ve seen a surge in 52-week new highs across countries and accelerating global advance/decline lines.

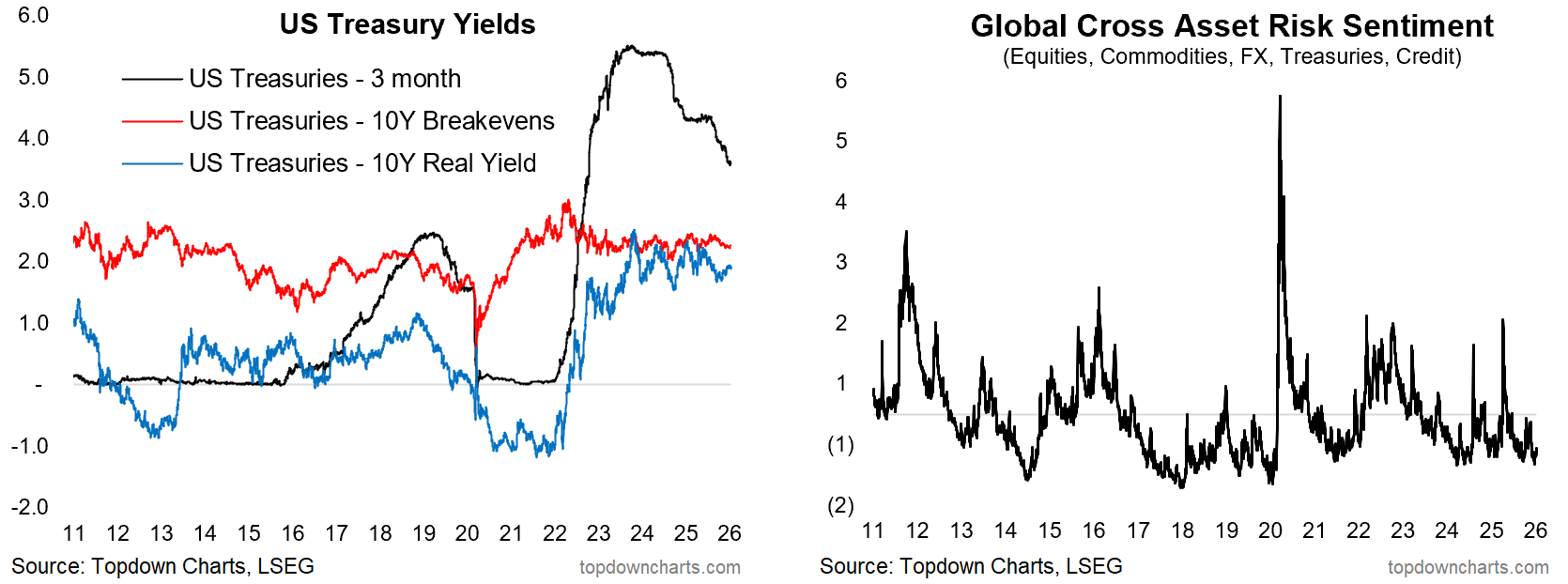

Treasury yields continue to consolidate, awaiting cue for next move from data. Risk pricing and credit spreads largely remain contained for now.

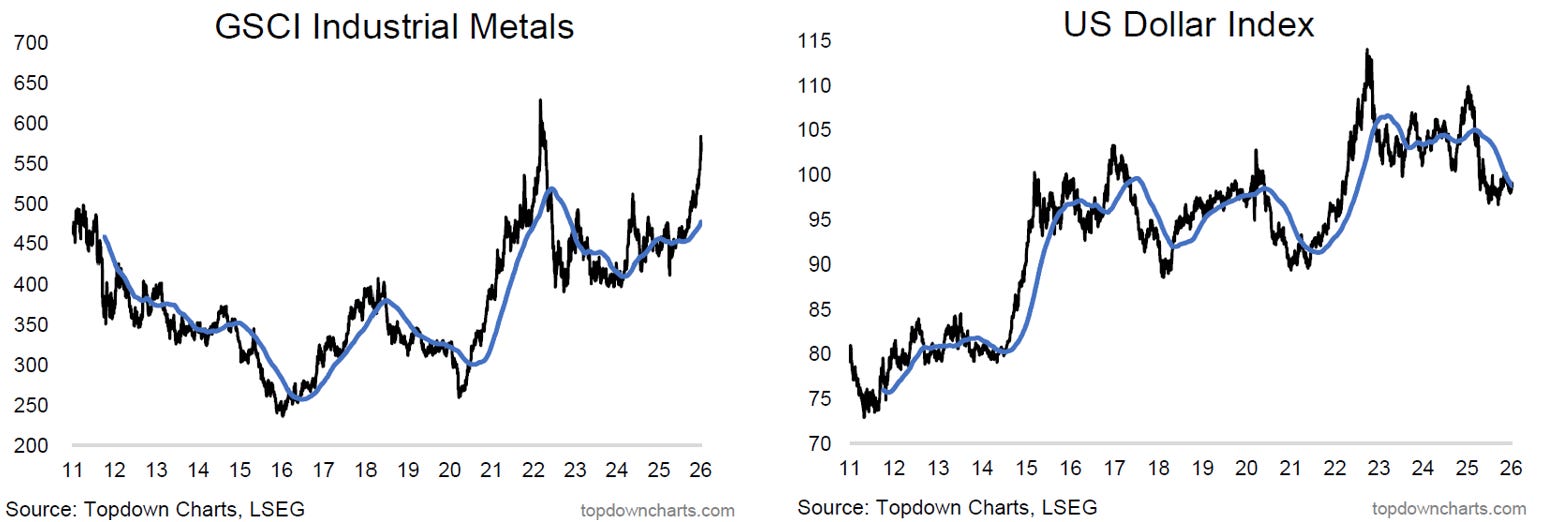

In FX, the DXY remains in a trading range; gearing up for next move. Commodities remain a mixed bag, but the key development has been the big breakout in industrial metals.

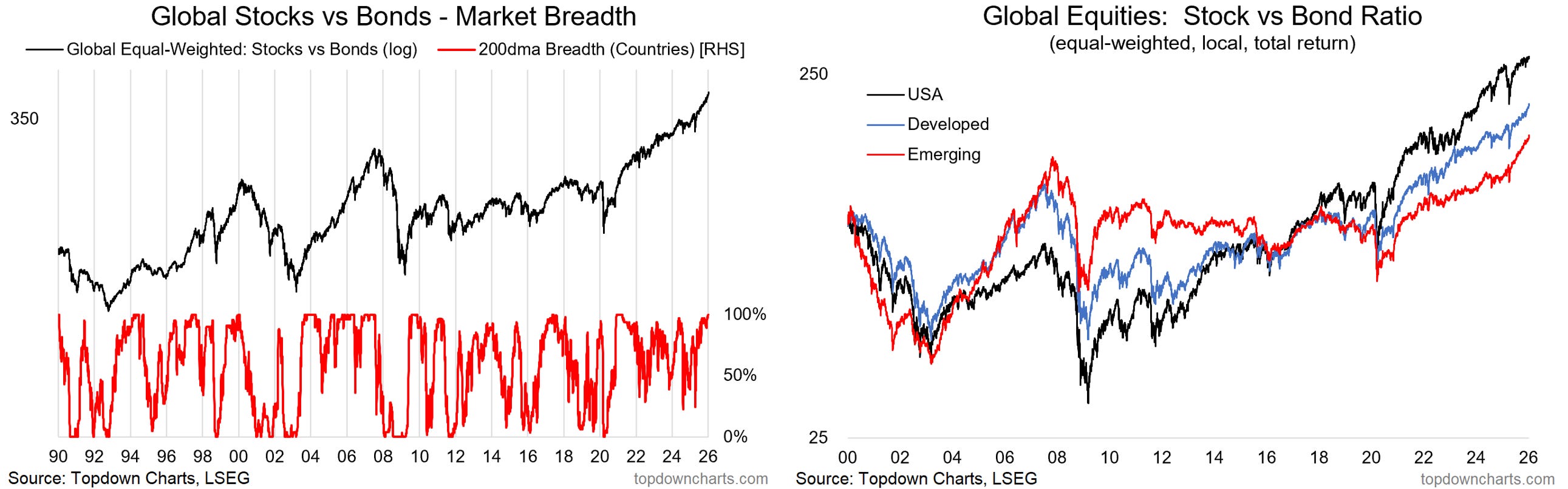

Market themes: Bullish Rotations...

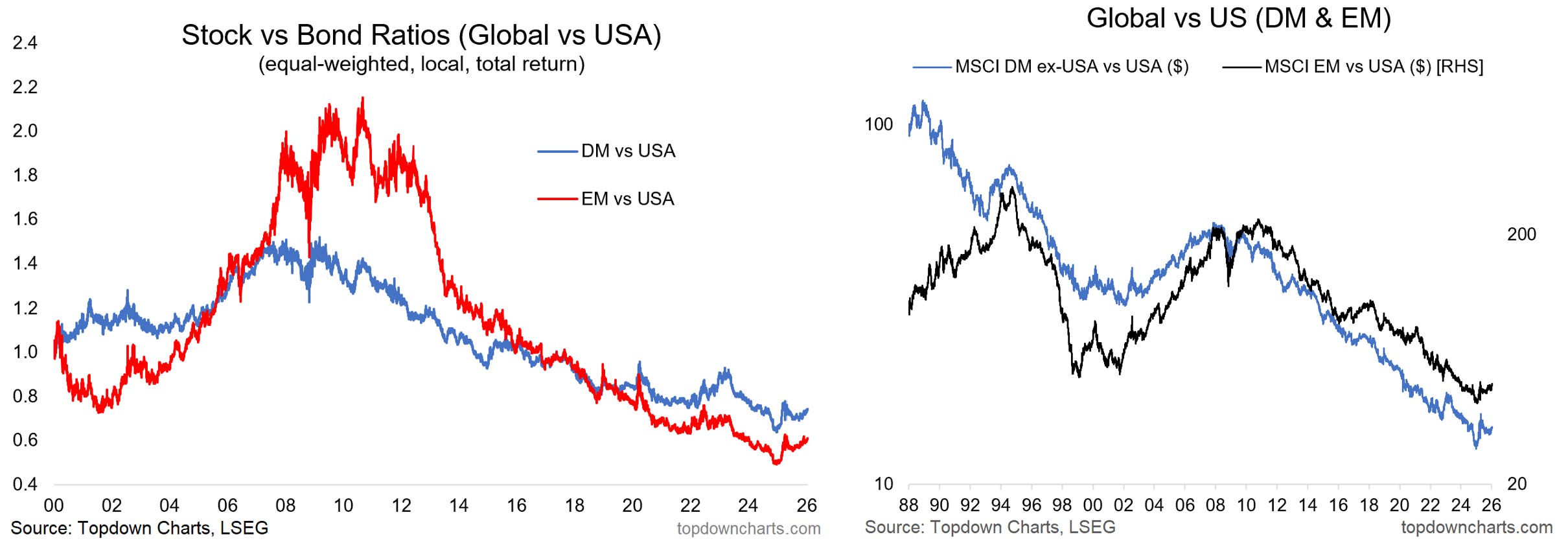

-Globally stocks are beating bonds.

--global stock/bond ratios are outpacing US stock/bond ratio

-Global stocks in general also beginning to outperform vs US stocks

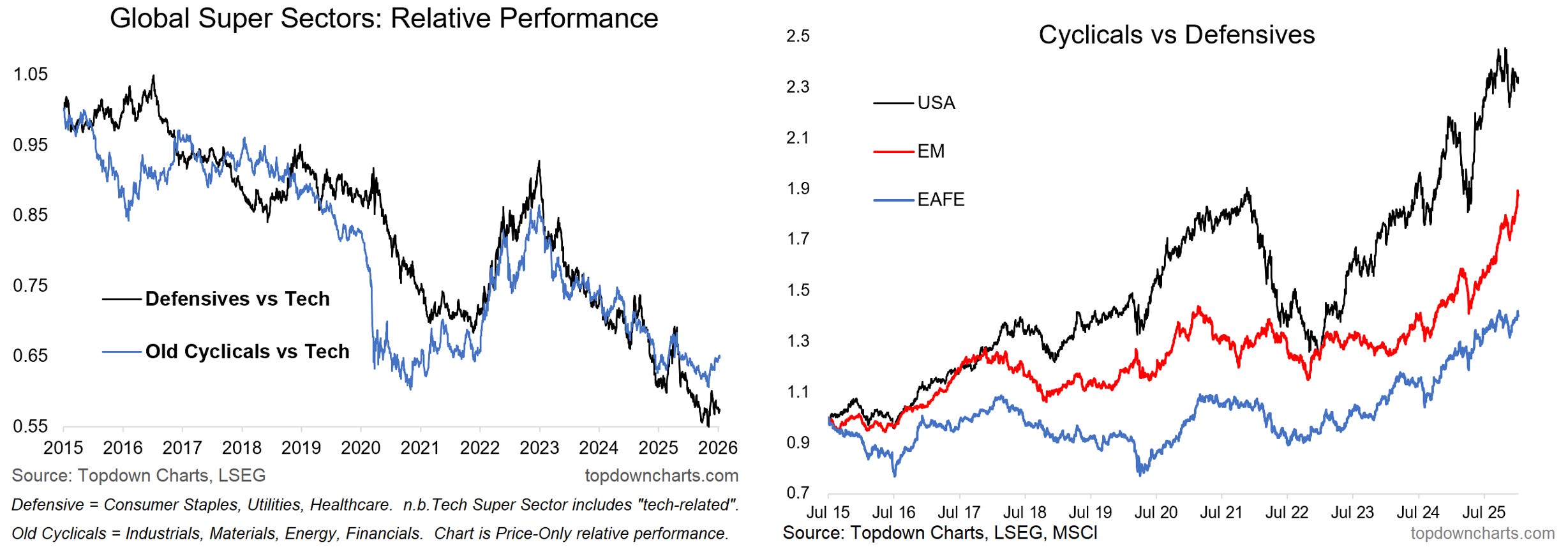

-Cyclicals ex-tech have been outperforming vs tech, and cyclicals generally outperforming defensives (especially EM)

--overall it’s consistent with bullish rotation, global growth acceleration, and bodes well for global ex-US equities outlook

Across global equities we are seeing a clear trend of stocks beating bonds, with the equal-weighted stock/bond ratio for EM + DM accelerating (consistent with risk-on, global growth acceleration, bullish rotation).

Further, both EM and DM stock/bond ratios are turning the corner vs USA (their stock bond ratios are rising at a faster pace vs US). This echoes the emerging trend we are seeing in pure equities relative performance for EM and DM vs US; these moves kicked-off in 2025 and could well go on to be a key theme for this year.

Within global equities we are seeing “Old Cyclicals” (basically cyclicals ex-tech) starting to outperform vs tech. Seeing cyclicals outperforming vs defensives particularly in EM but also to a lesser extent in DM.

Overall this set of charts is consistent with bullish rotation across sectors, countries, and asset classes; bodes well for global equities ex-US.

Macro & Markets: This week we get China M2/new loans, and from the US: CPI/PPI, NFIB, Philly Fed, NAHB (so an interesting data week, but also plenty going on in geopolitics e.g. Iran, Europe).

In markets, the US 10yr yield remains locked in a tight range, DXY extending rally off support, gold pressuring resistance ~4500, WTI crude oil rebounding off a higher s/t low, stocks breaking higher…

Research Agenda: Back into the Weekly Macro Themes reports this week!

And, in case you missed it -- the Quarterly Strategy Pack was sent out last week.

>> Quarterly Pack ZOOM WEBINAR DETAILS (please register using the relevant link below)

New York -- 4pm Tuesday, 13th January https://us06web.zoom.us/meeting/register/DX9kv3wLTiubg8Wxq0rbAA

London -- 8am Wednesday, 14th January https://us06web.zoom.us/meeting/register/m5jCJfRsR1y_8HodtpT7vA

Best regards,

Callum

Best regards,

Callum Thomas

Head of Research | Topdown Charts Limited | www.topdowncharts.com

Mobile: (+64) 22 378 1552

Email: callum.thomas@topdowncharts.com