Hello and welcome to a new week - hope you have a good one!

The latest Global Cross Asset Market Monitor [Market Chart Pack] is attached below:

Topdown Charts Global Cross Asset Market Monitor 19012026

Global Markets Monitor -- Notable Developments

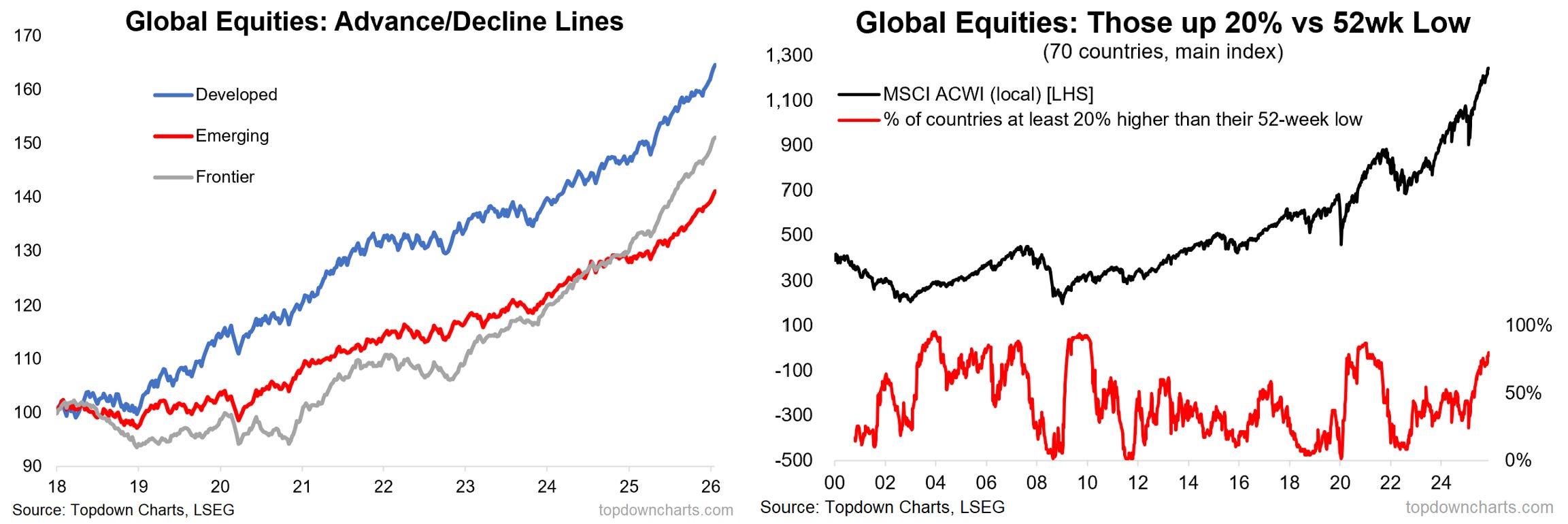

Stocks broadly stronger last week, especially global (non-US). On sectors, materials and industrials gaining significant ground, tech and defensives lagging.

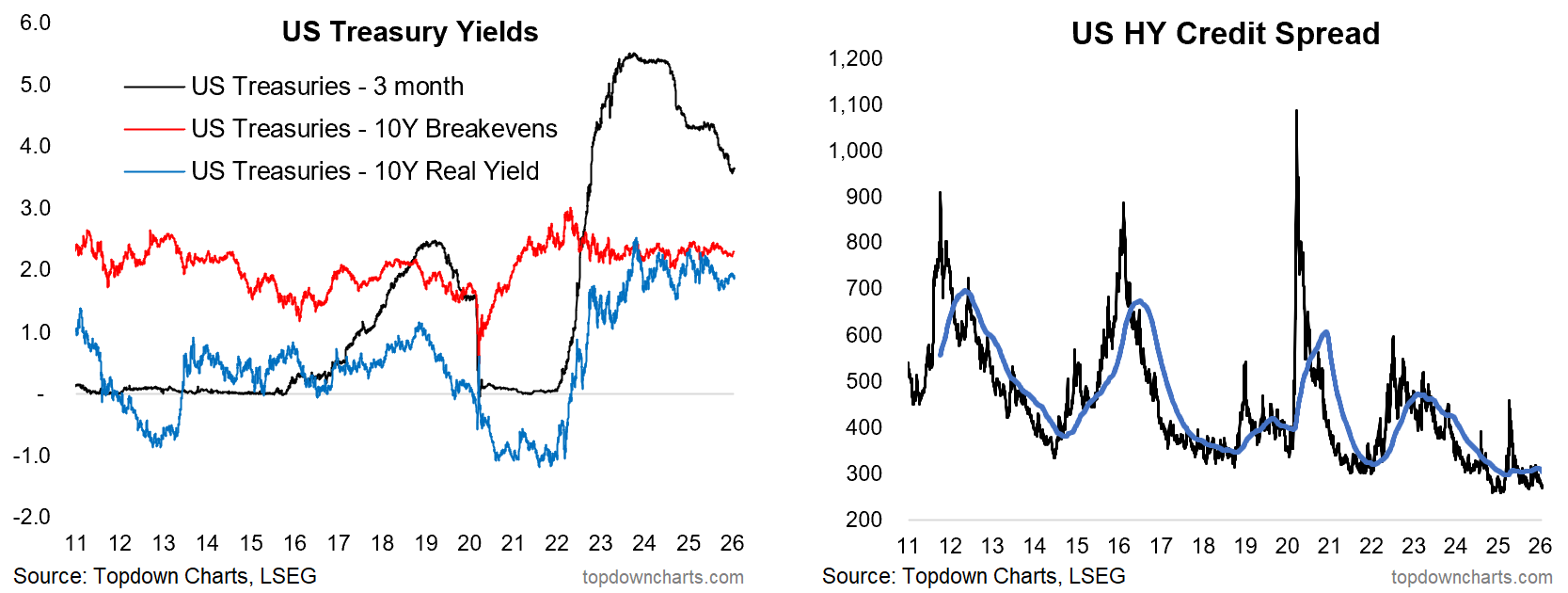

Treasury yields basing across the curve (short-term rates stopped going down), breakevens ticking up slightly. CDS/Credit spreads probing the lows.

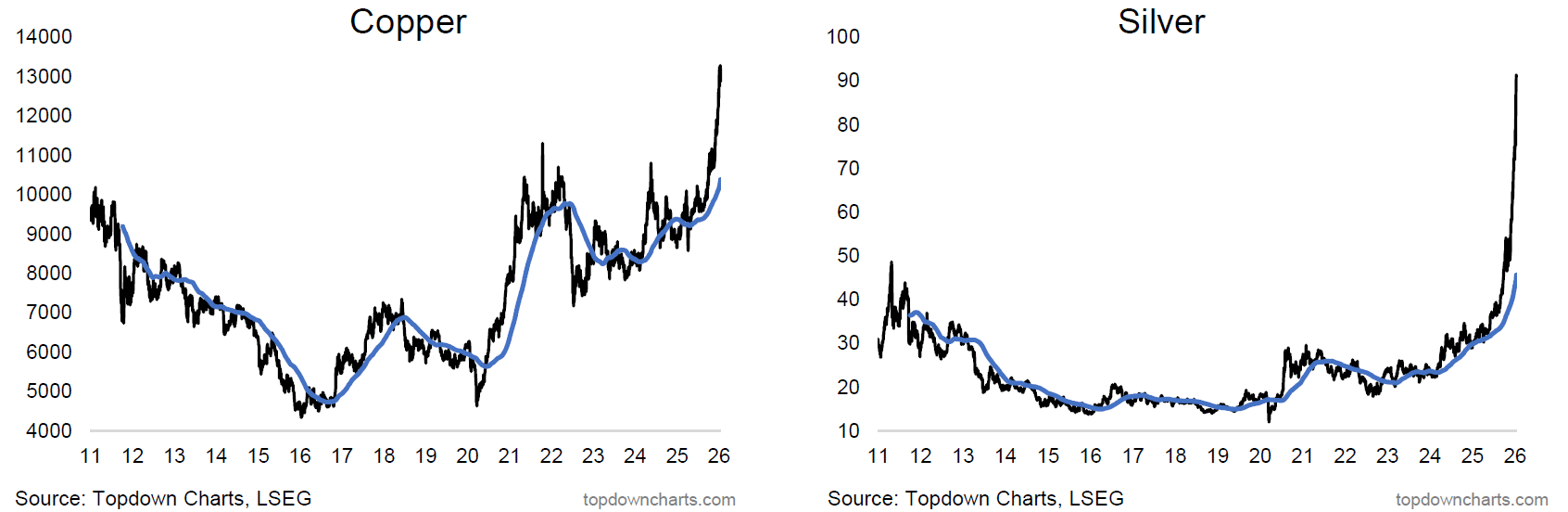

In FX, the DXY remains range-bound for now, likewise Asian/EMFX in consolidation mode. Commodities remain a mixed bag with industrial and precious metals largely stronger, energy and oil prices particularly volatile, and agri/livestock also mixed-weaker.

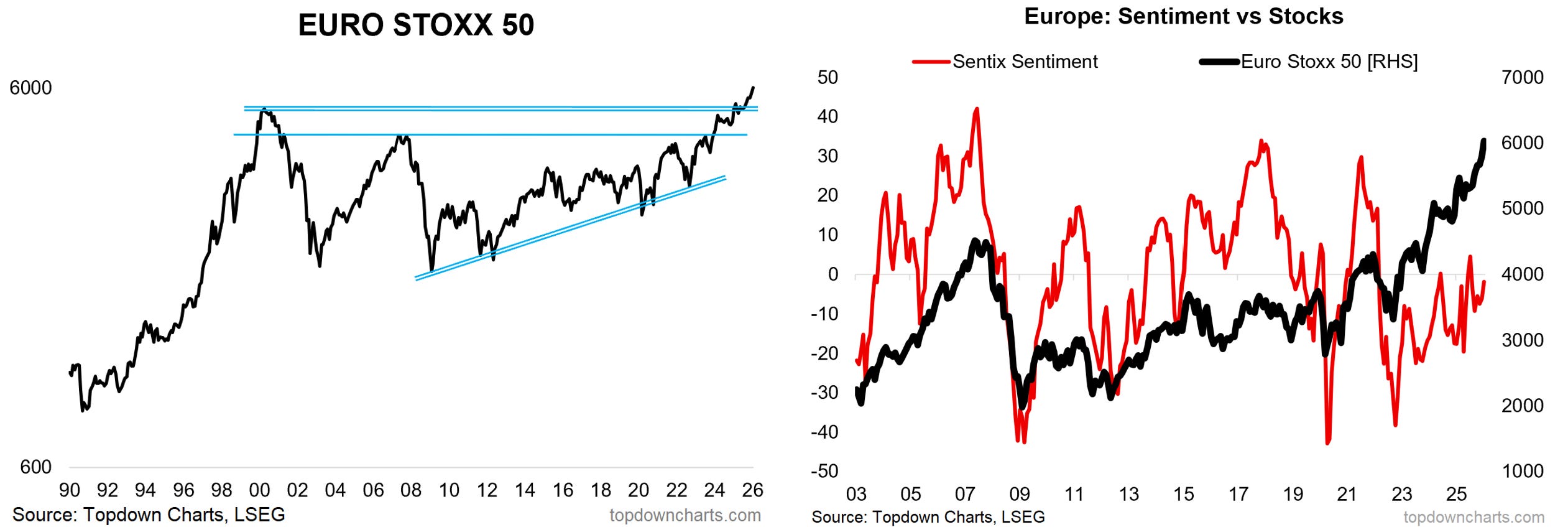

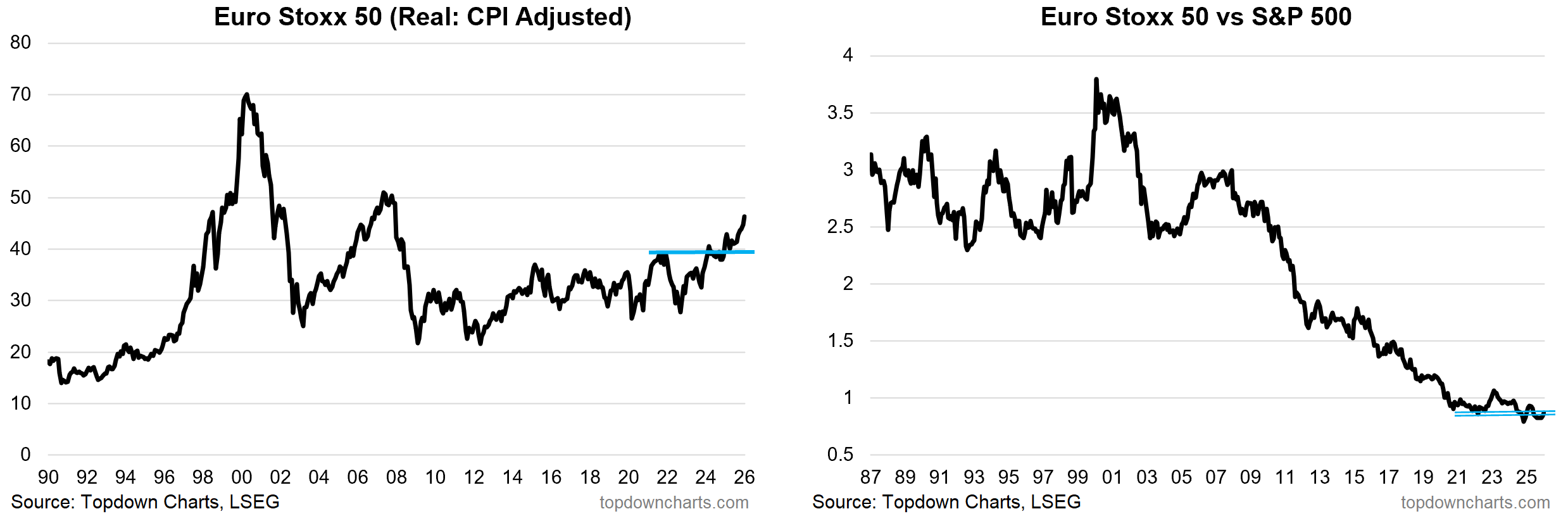

Market themes: European Equities...

-European stocks continue to trend higher post-breakout.

--Sentiment remains pessimistic; which is helping contribute to the upside.

--In real CPI adjusted terms the breakout also looks good (albeit still much lower than previous peaks

--Relative to US stocks Europe remains range-bound.

-While geopolitical risk remains a big issue (e.g. the weekend developments), there are a lot of favorable factors that likely help driver further follow-through here.

Although the latest Trump-talk this weekend likely rattles things when markets open again, European equities have been pushing onwards to fresh new highs --following on from their big breakout last year. Sentiment meanwhile remains pessimistic (which of course is supporting the moves as it represents many minds that are slowly changing to the bullish side), with geopolitical concerns weighing.

Adjusted for CPI, the breakout in European stocks is also compelling; particularly coming after such a long period of ranging -- yet in real terms the index remains far below the previous peaks. Relative to US stocks, it’s still a work in progress in terms of breaking out of the lows; and on this note, European stocks continue to trade at near-record cheap relative value discounts vs US stocks.

With the prospect of stronger global growth, monetary tailwinds, cheap valuations, and rotation (growth to value, US to global), European stocks likely have plenty of room to run.

Macro & Markets: This week we get China Dec/Q4 data, WEF, BOJ rate decision, and a timely macro update from the January flash PMIs. It’s also a shortened weak in the USA with MLK day Monday.

In markets, US 10yr yield is attempting to break higher, DXY pressuring resistance, gold continuing to trend higher, WTI crude oil back to support, stocks consolidating…

Research Agenda: This week I’ll be looking into fixed income and global equities.

And, in case you missed it -- the key conclusions from the latest Weekly Macro Themes report (let me know if you did not receive it):

1. US Dollar: Remain bearish medium/longer-term given expensive valuations, fading yield support, longer-term technicals, but wary of short-term upsides (sentiment, positioning, seasonality, technicals).

2. EM Equities: Remain bullish emerging market equities given supportive valuations, monetary tailwinds, improving earnings outlook, light allocations, and strong technicals.

3. China Equities: Remain bullish Chinese stocks given strong technicals, supportive valuations, improving sentiment, and mild but gathering macro/monetary tailwinds.

4. Commodities: Remain bullish commodities given cheap valuations, supply tailwinds, improving macro-fundamentals, light allocations, skeptical sentiment, strong technicals.

5. Commodity Equities: Remain bullish given strong technicals, bullish outlook for commodity prices, wary of rising valuations (especially precious metal stocks); but clear scope for upside.

ALSO — Q1 Strategy Pack Webinar replay:

Best regards,

Callum Thomas

Head of Research | Topdown Charts Limited | www.topdowncharts.com

Mobile: (+64) 22 378 1552

Email: callum.thomas@topdowncharts.com