Hello and welcome to a new week - hope you have a good one!

Please also take a minute to fill in the client survey (how you rate the key reports and overall service):

The latest Global Cross Asset Market Monitor [Market Chart Pack] is attached below:

Topdown Charts Global Cross Asset Market Monitor 02032026

Global Markets Monitor -- Notable Developments

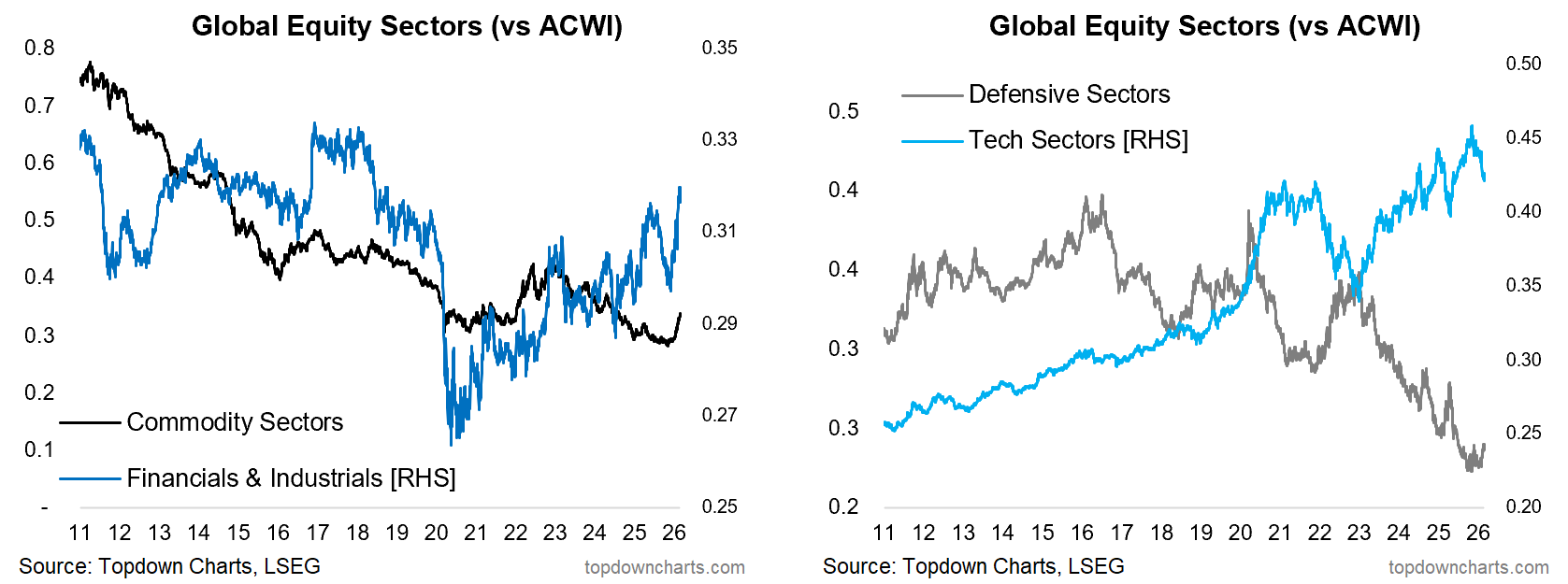

Rotation remained the key theme last week with global/ex-tech (especially hard cyclicals: industrials, energy, materials) performing well, and US/tech weaker.

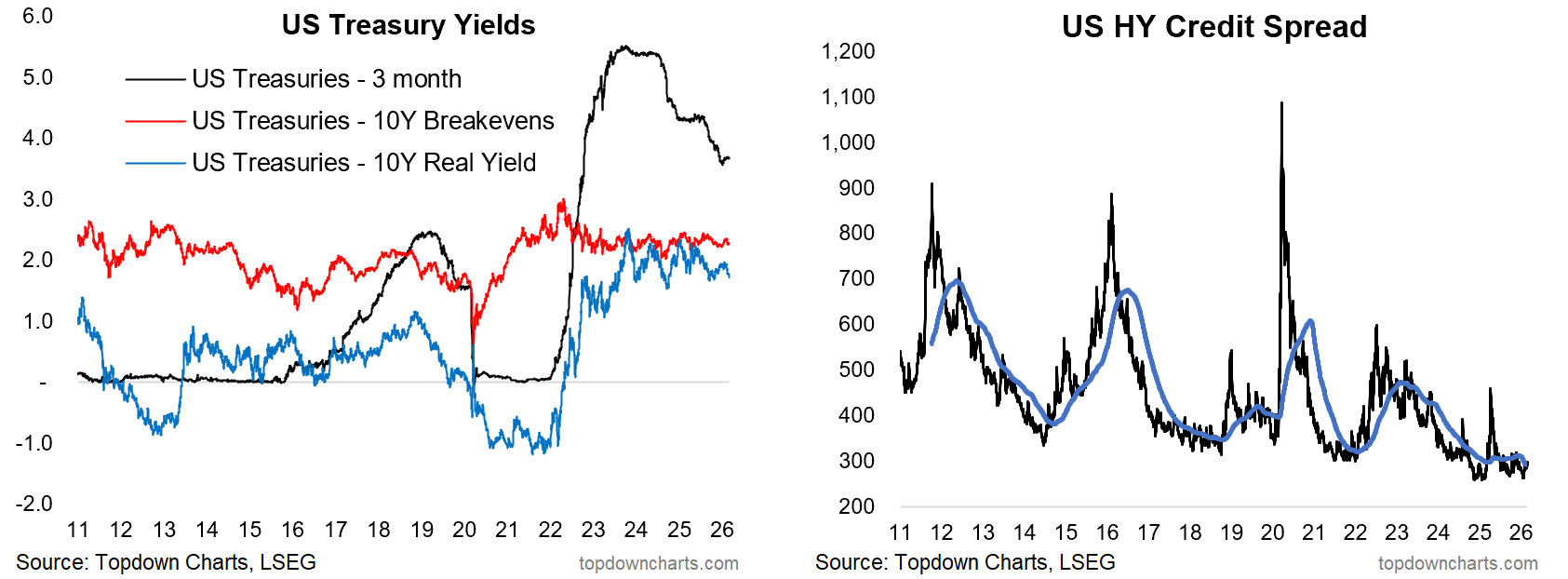

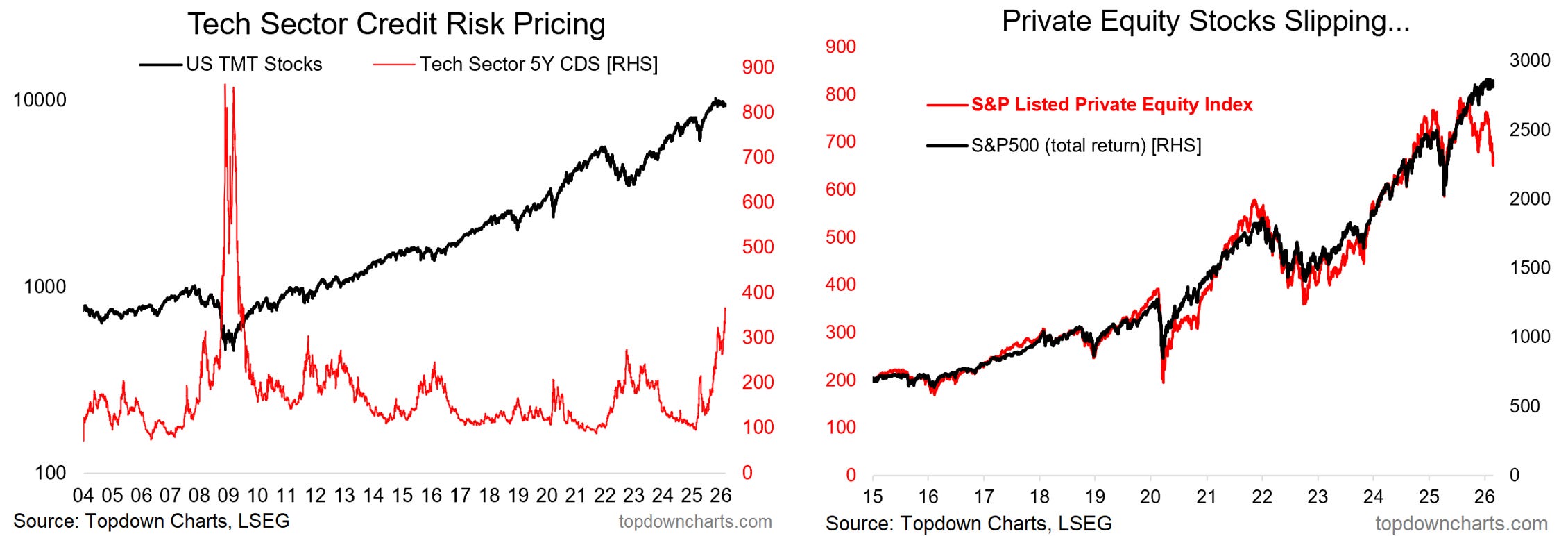

In fixed income, US treasury yields ticked lower (likewise developed 10yr govt yields), and US credit spreads/CDS ticked up off the lows.

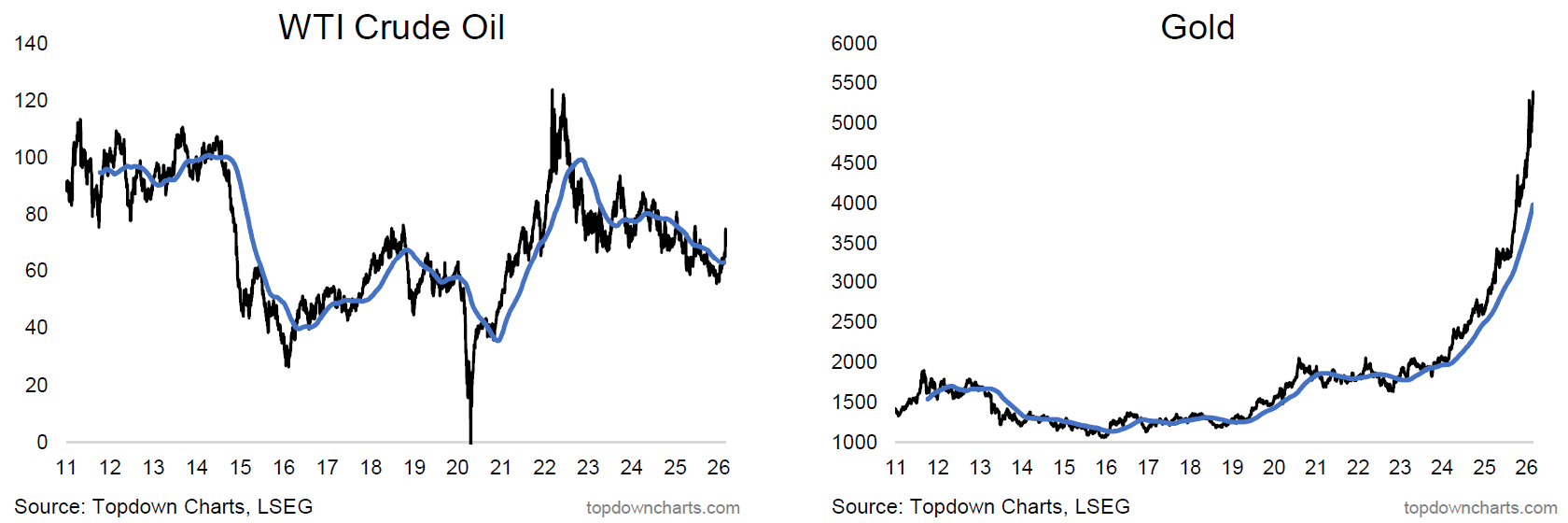

FX markets remain in a bit of a stalemate with previous USD weakness pausing, but ongoing strength in Asian/EMFX especially CNY. Commodities remain a mixed bag, industrial metals consolidating, precious metals pushing higher, energy elevated and agri mixed.

Market themes: Market Risk...

-Geopolitics rarely have a lasting impact on the stockmarket, unless it damages the macro or comes on top of other issues.

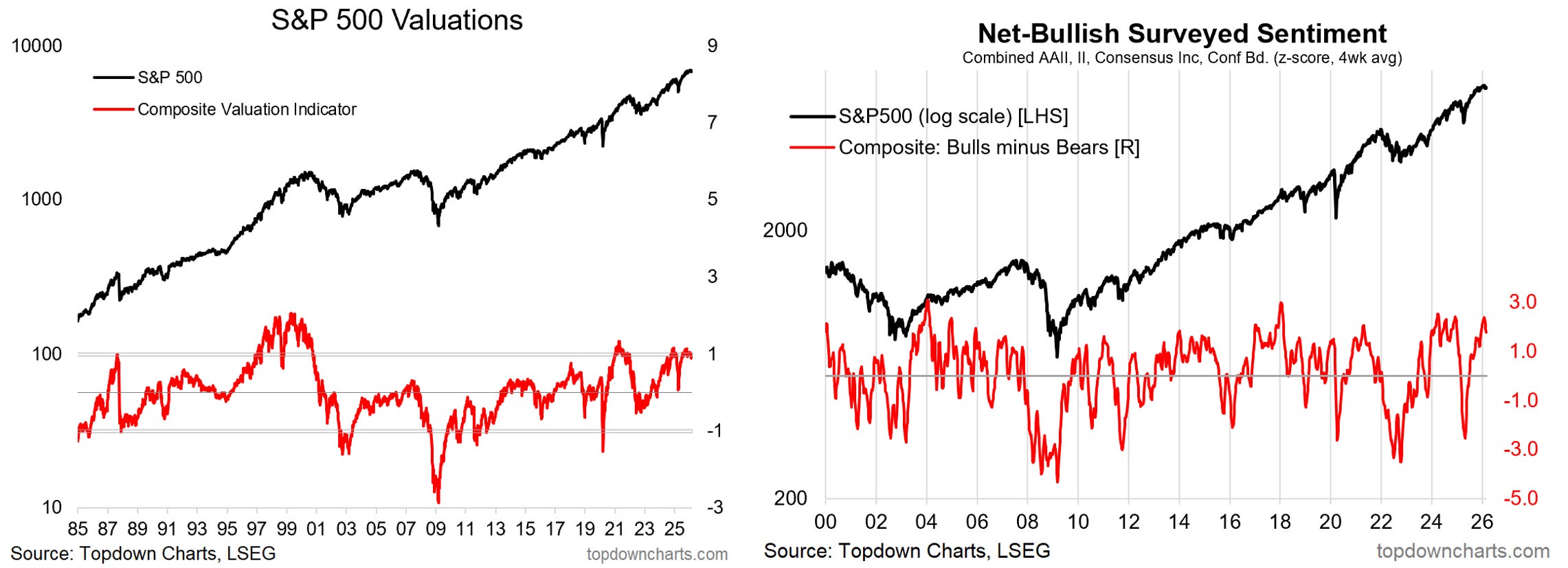

-There is some vulnerability for US stocks as valuations and sentiment are rolling over from overvalued/overhyped conditions (especially tech), so it warrants close monitoring.

-But there are some offsetting factors.

I don’t have much to add on Iran/geopolitics specifically, but in general geopolitical events normally don’t tend to have much enduring impact on the stockmarket beyond the short-term spooky/scary effects unless they really damage the macro in a meaningful way... or if they turn up at the wrong time (e.g. if there were already issues, market was rolling over from stretched conditions). For example, in 2022 the Russian invasion of Ukraine catalyzed the beginning of a bear market, but it came as the market already peaked from overhyped/overvalued conditions in late-2021... and specifically it featured a commodity price spike due to direct effects of the conflict and the sanctions reaction (which drove up already rising inflation and rates).

In the current context, there are actually some parallels e.g. sentiment and valuations rolling over from overhyped and overvalued levels. This means the market is perhaps more sensitive and at risk of downside, but again I think we’d probably need to see the macro damaged from an enduring spike in energy prices and disruption to global trade flows (hard to say at this point, it is a risk, but no firm evidence for this as yet).

The more concerning aspect is that tech stocks have already peaked from overvalued and overhyped starting conditions, and so I would continue to be focused more on that, but also factoring in the risk of oil shock issues.

Having said that, the market had already been pricing in some risk of Iran strikes, so part of that uncertainty has been resolved, and we are seeing the bullish rotation trade (strong absolute and relative performance from cyclicals/global/value/small -- picking up the slack from weakness in tech stocks, and reflecting macro-fundamental improvements). So I don’t think we necessarily panic or go full-bear just yet, as there are offsetting factors. Continuing to monitor the situation.

Macro & Markets: This week we get Feb PMIs and payrolls.

In markets, the US 10yr yield is breaking lower, DXY drifting higher, gold extending rally, WTI crude making initial spike higher on Iran developments, Bitcoin mixed-volatile, stocks mixed (tech lackluster, cyclical/value stronger).

Research Agenda: This week I’m working on the monthly pack.

And, in case you missed it -- the key conclusions from the latest Weekly Macro Themes report (let me know if you did not receive it):

1. GSV vs ULG: remain bullish Global/Small/Value vs US/Large/Growth on absolute and relative valuations (with ample room to run), and notably improved technicals.

2. EM Equities: remain bullish EM equities given strong technicals, breakout in earnings, and strong cyclical momentum overall, but wary of stretched sentiment (+valuations no longer cheap).

3. EM Fixed Income: remain low-conviction bullish on EM sovereign bonds given cheap valuations, improving sentiment/technicals, monetary tailwinds (for now), and benign macro-risk backdrop.

4. EMFX: the improving outlook for EMFX (cheap valuations, improved technicals) is helping reinforce strength in EM equities and EM local currency bonds.

5. Frontier Markets: monitoring situation as valuations are getting expensive (+technical risk flags), but for now still seeing strong bullish momentum and monetary tailwinds.

Best regards,

Callum Thomas

Head of Research | Topdown Charts Limited | www.topdowncharts.com

Mobile: (+64) 22 378 1552

Email: callum.thomas@topdowncharts.com