Hello and welcome to a new week - hope you have a good one!

The latest Global Cross Asset Market Monitor [Market Chart Pack] is attached below:

Topdown Charts Global Cross Asset Market Monitor 09022026

Global Markets Monitor -- Notable Developments

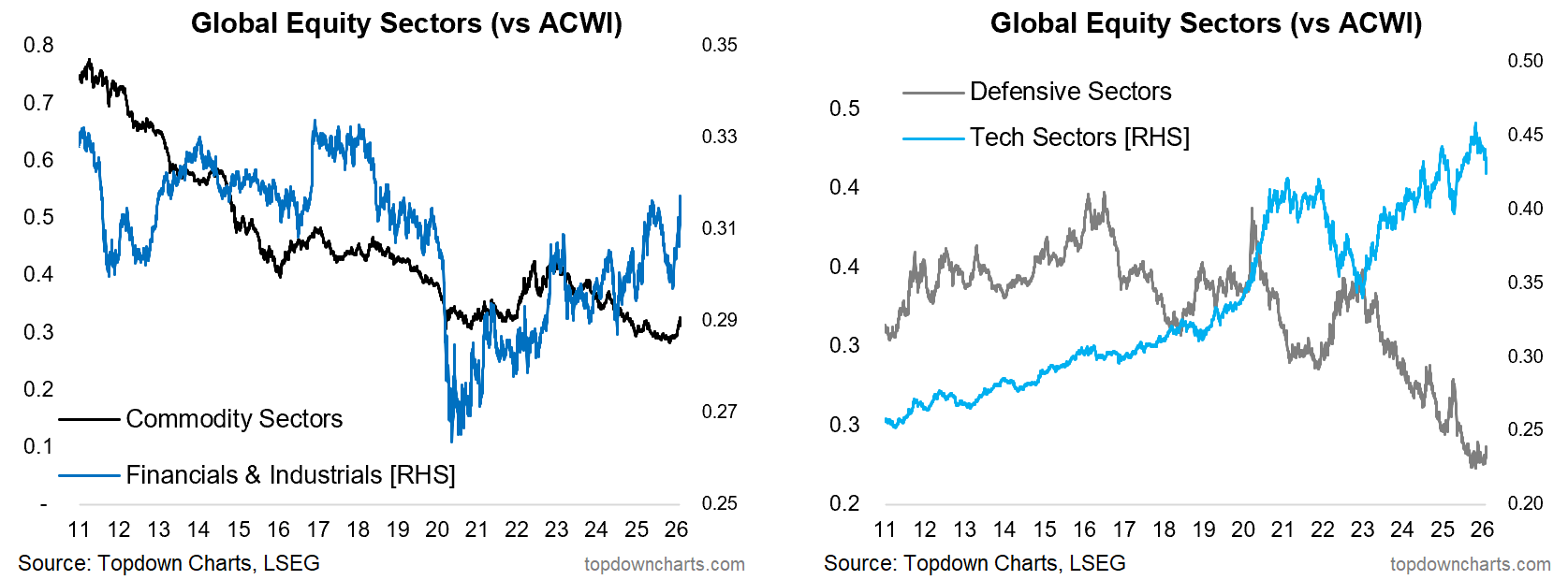

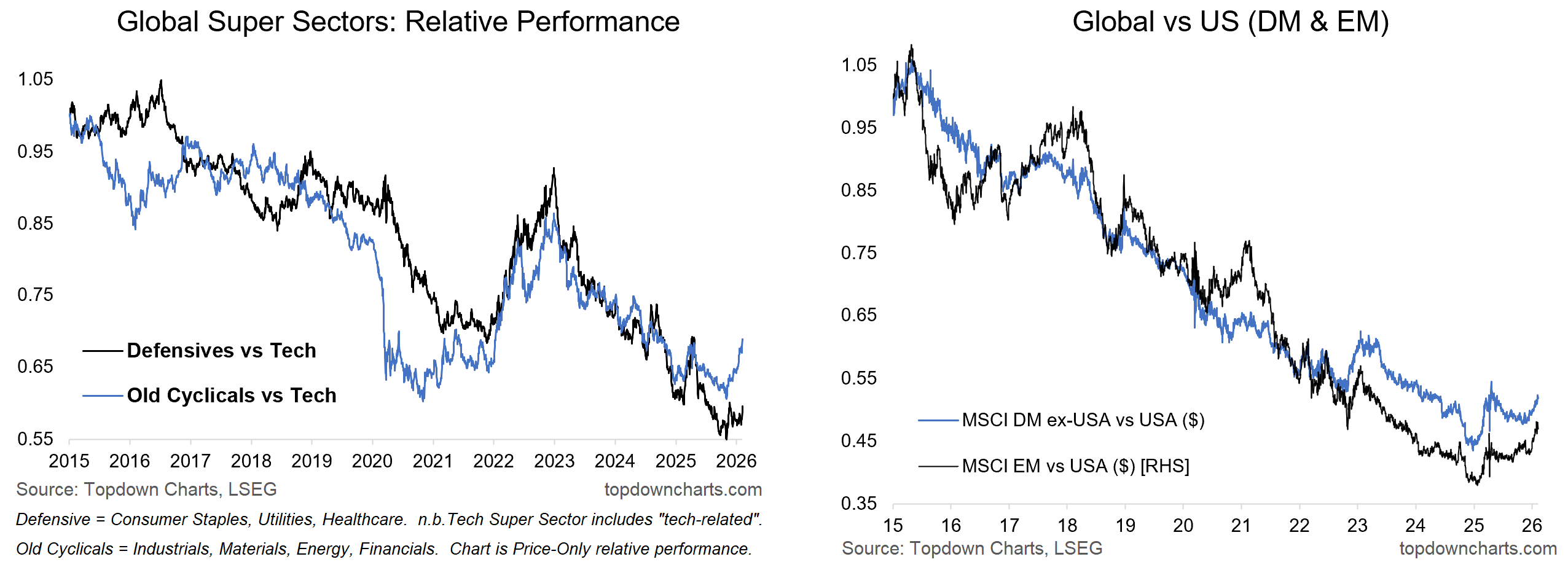

Stocks were somewhat volatile last week, with rotation a key theme. On the sector front, tech and consumer discretionary have been losing ground, while traditional cyclicals have been gaining, and defensives mixed (staples gaining ground). Global stocks continue to gain vs US.

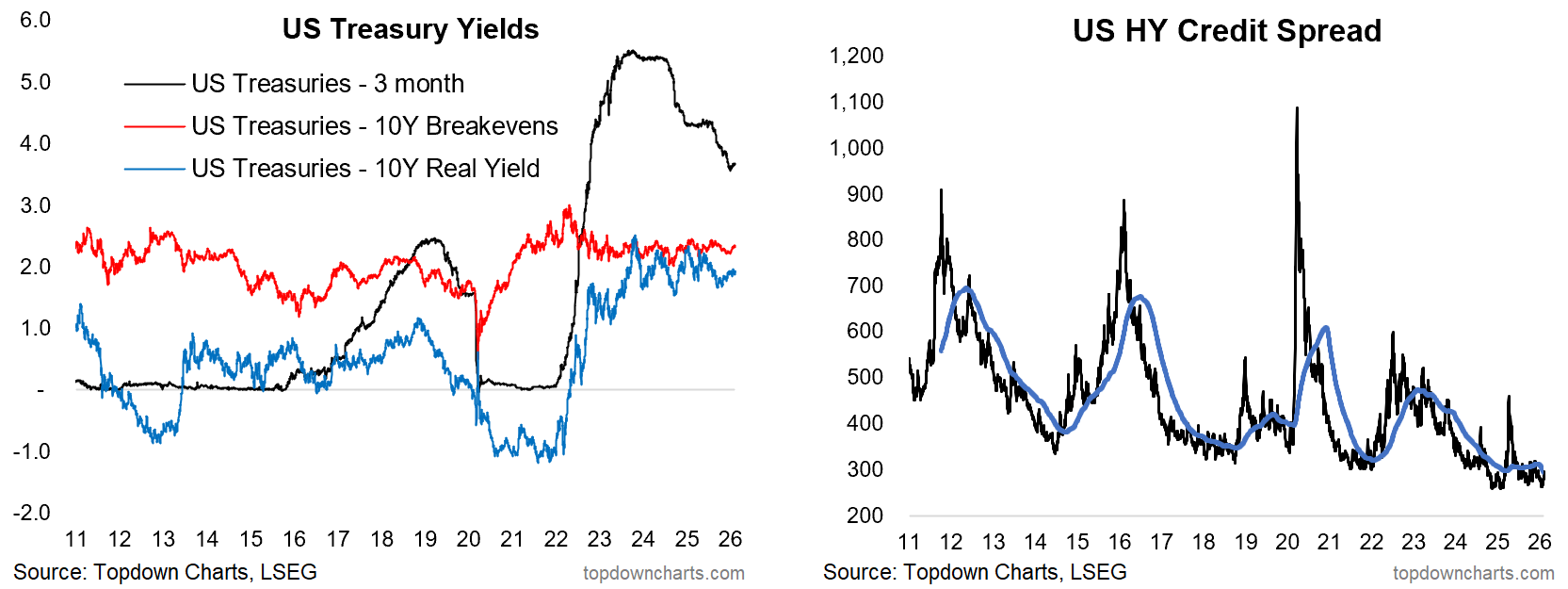

On the fixed income front, treasury yields remain largely in a holding pattern following the initial bounce off the lows. US credit spreads moved slightly higher off the lows.

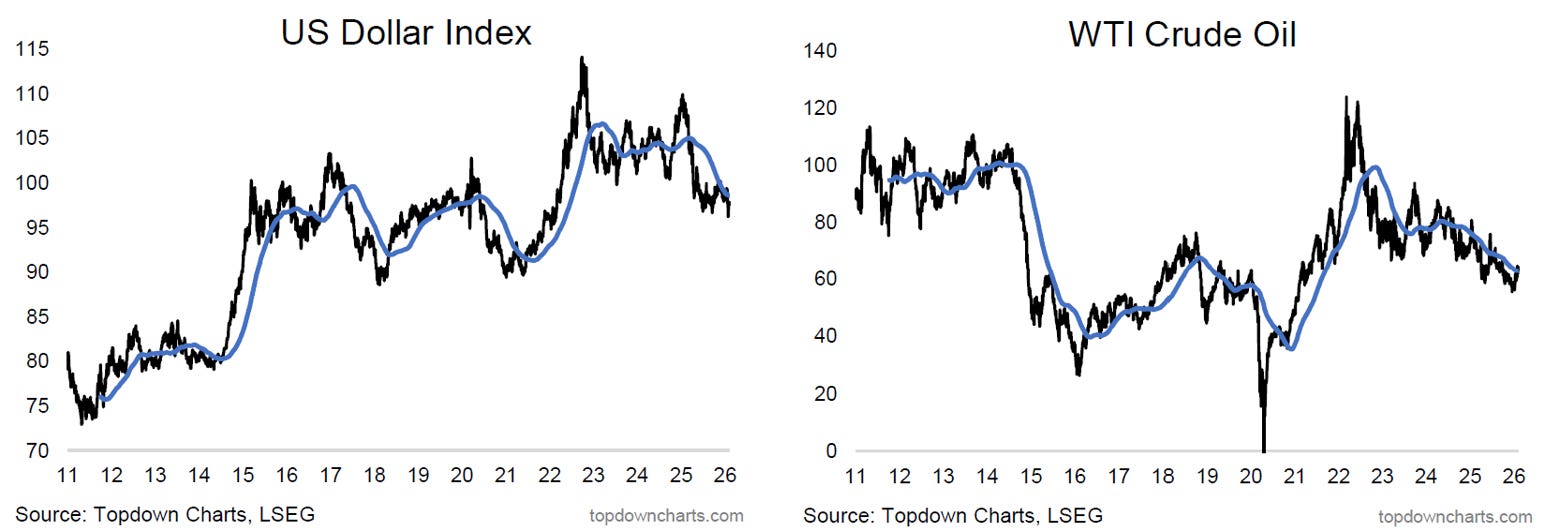

In FX, the US dollar remains under pressure, Asian/EMFX on an improving path. Commodities remain a volatile and mixed bag, crude oil consolidating, precious metals finding support, agri mixed, industrial metals trending higher.

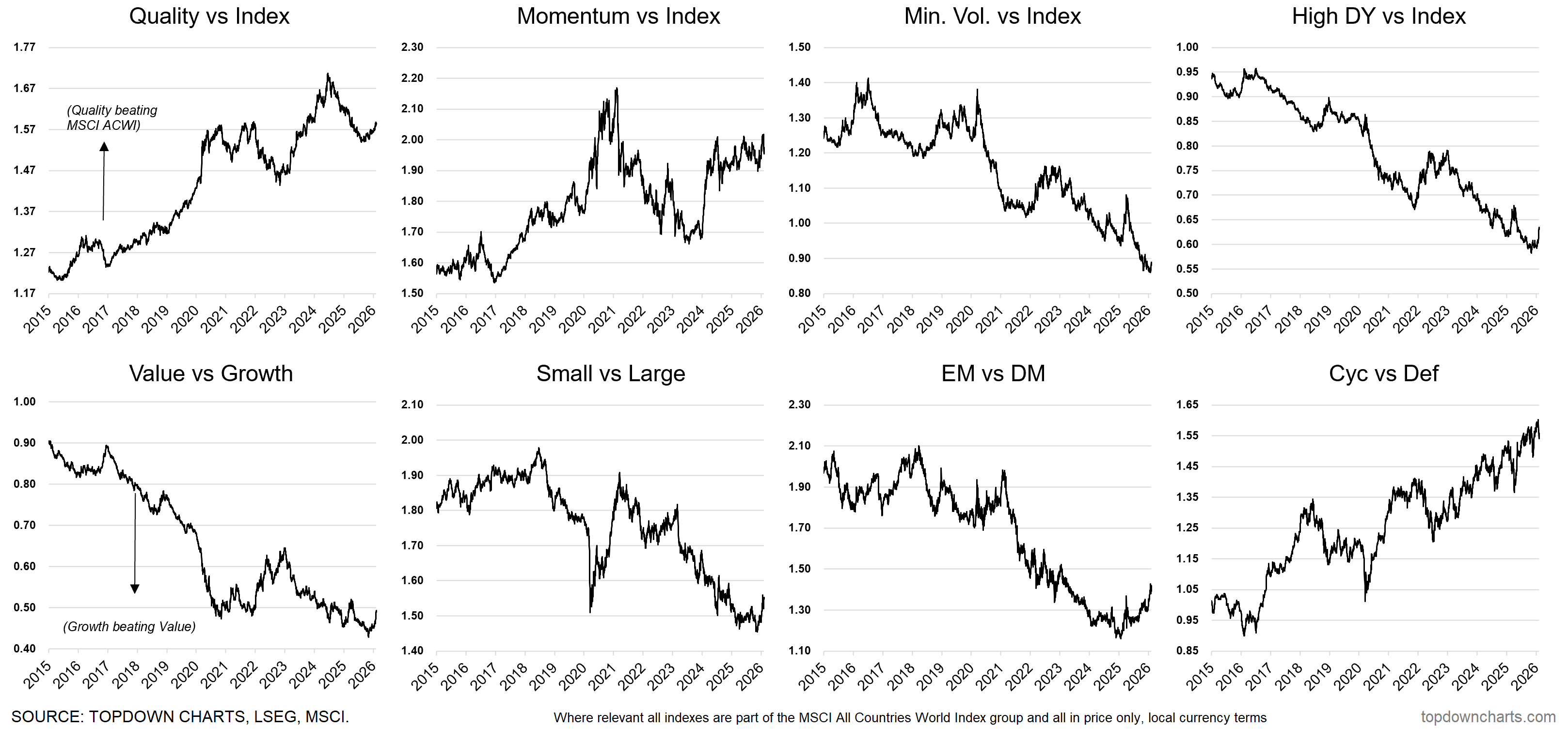

Market themes: Global Equity Rotation...

-Rotation is the word of the year so far for stocks.

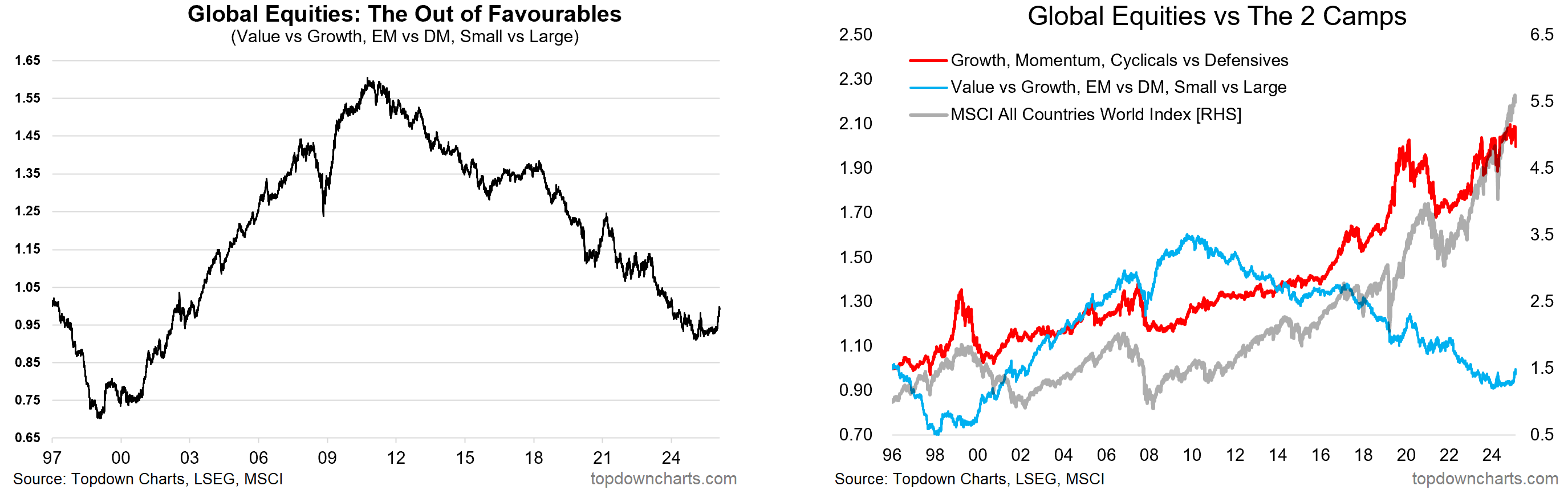

-Seeing previous out-of-favour pairs moving the most (value vs growth, small vs large, EM vs DM).

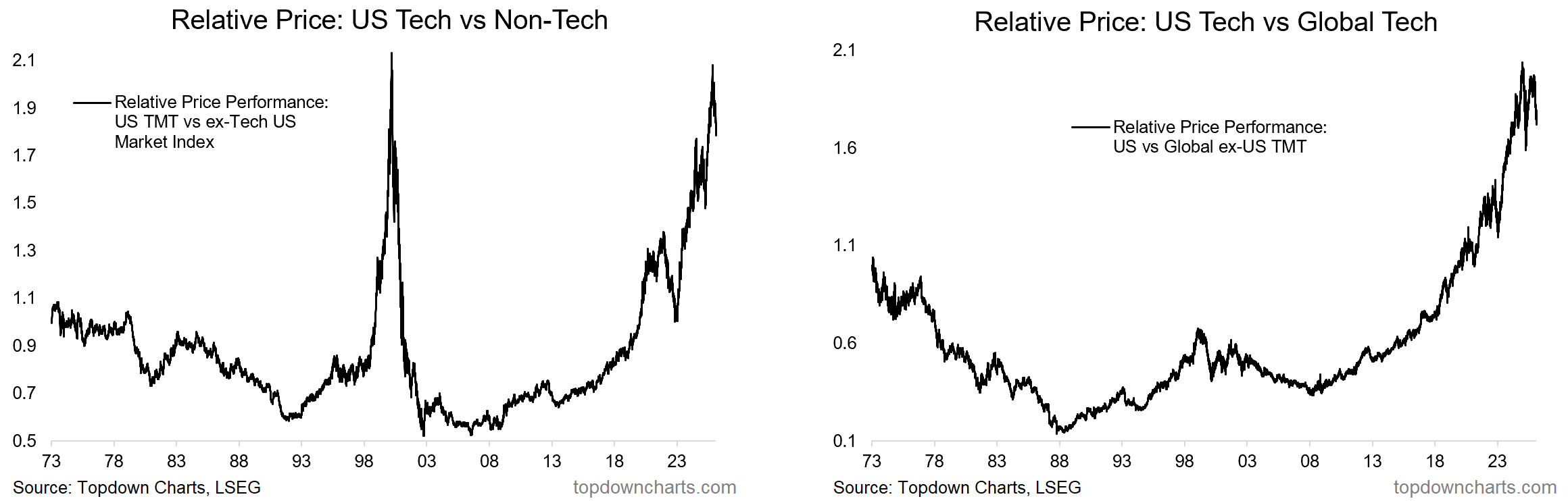

-A key element has been the peak in (US) Tech in both absolute and relative terms, and there’s a decent chance we see a continuation of these recent trends.

The standouts in styles/factors have been quality, high dividend yield, value vs growth, small vs large, and EM vs DM.

The rotation trade has been most noticeable and most notable in the 3 key pairs that have seen the longest and most extended moves, namely; value vs growth, EM vs DM, small vs large -- basically the long-standing out of favourables. The sharp move in the combined line for those 3 is significant given it comes after a long-term downtrend. But also in so far as it might signal a change in market leadership -- this can have bearish implications for global equities e.g. the unwinding of the dot com bubble, but we have seen this group carry the market higher before e.g. just after the 08 crash, and briefly in 2021.

Looking at it from a sectors angle, both cyclicals and defensives have turned up vs tech; notably ex-tech cyclicals (industrials, materials, energy, financials) have staged a particularly sharp rally vs tech. Meanwhile both EM and DM have been gaining ground vs US stocks.

Staying with tech, the big story has been US tech topping in both absolute and especially relative terms. US tech has taken a tumble vs US non-tech and global ex-US tech after extended exponential runs on both fronts.

Given this is also occurring alongside stretched absolute and relative valuations for US tech, it is something to keep an eye on from a risk perspective, but also as a source of potential further rotation flows, if investors start giving up on tech and looking elsewhere for gains.

Macro & Markets: This week we get China M2/new loans and CPI/PPI, US NFIB small business confidence, delayed Jan payrolls release, and CPI.

In markets, US 10yr yield still in consolidation mode, DXY hovering around support, gold regaining momentum around 5k, WTI crude back to support, Bitcoin initial rebound from precipitous declines of the past week, stocks rebounding off support…

Research Agenda: I’ll be looking into credit spreads, EM fixed income, tech stocks, and agri commodities, among other things this week.

And, in case you missed it -- the January monthly pack was sent out last week.

Best regards,

Callum Thomas

Head of Research | Topdown Charts Limited | www.topdowncharts.com

Mobile: (+64) 22 378 1552

Email: callum.thomas@topdowncharts.com