Hello and welcome to a new week - hope you have a good one!

The latest Global Cross Asset Market Monitor [Market Chart Pack] is attached below:

Topdown Charts Global Cross Asset Market Monitor 05012026

Global Markets Monitor -- Notable Developments

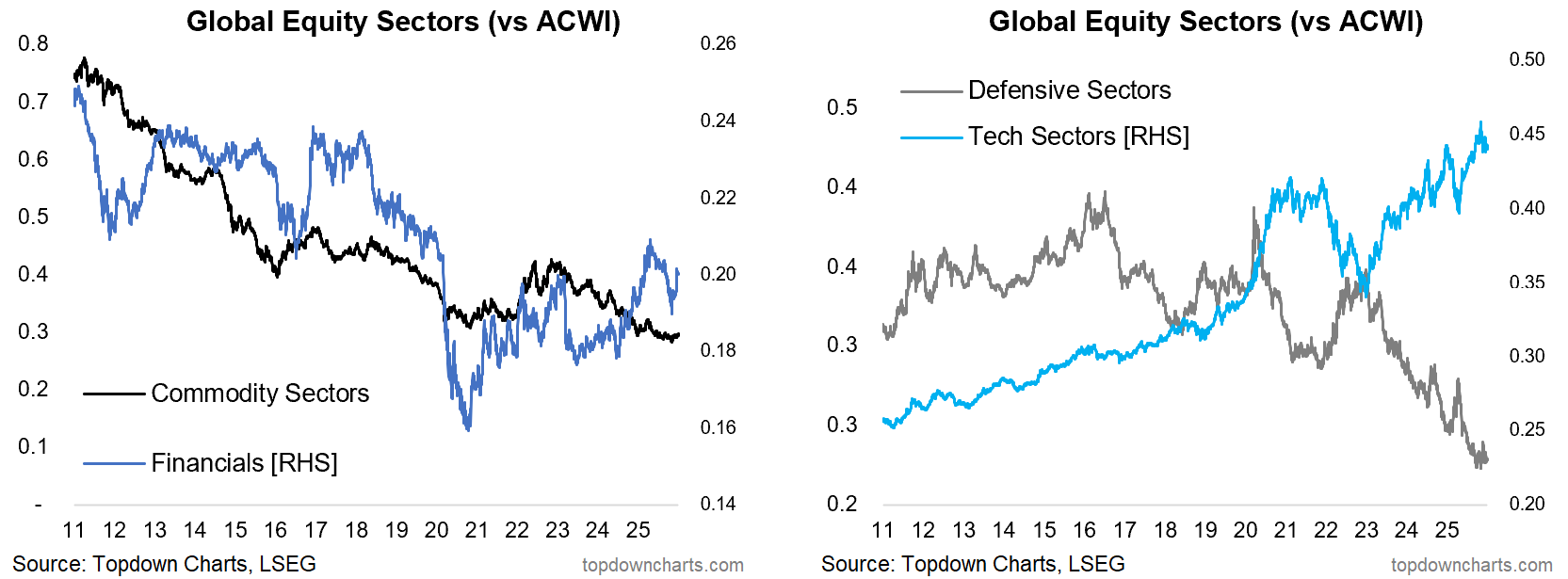

Stocks were largely stronger last week, particularly global ex-US. On the sector front, tech and tech related sectors have peaked in relative terms for now, defensives have bottomed in relative terms but yet to really turn the corner, meanwhile financials + industrials have gained back ground, and commodity sectors are gaining (mostly materials/miners).

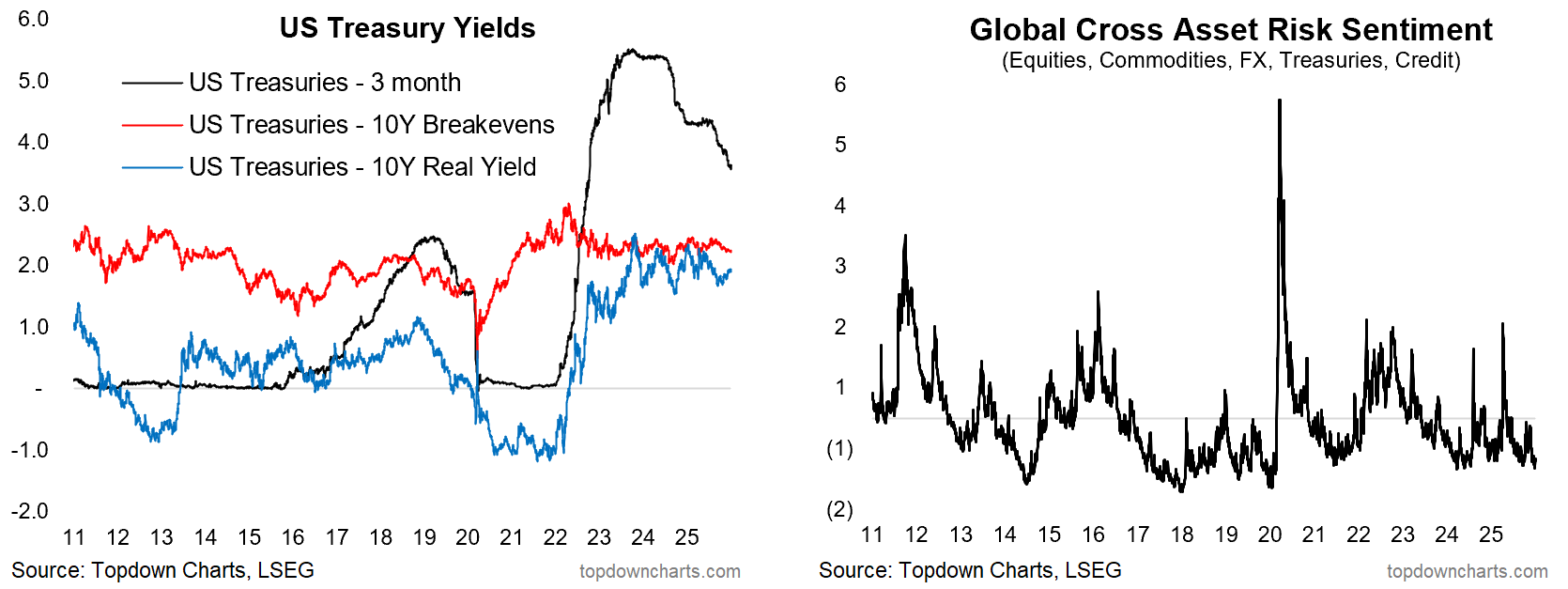

In fixed income, short-term rates continue to lean lower, while longer-end yields are consolidating-to-slightly higher (and yield curve ticking up). CDS/Credit spreads and risk pricing in general remains well-contained for now.

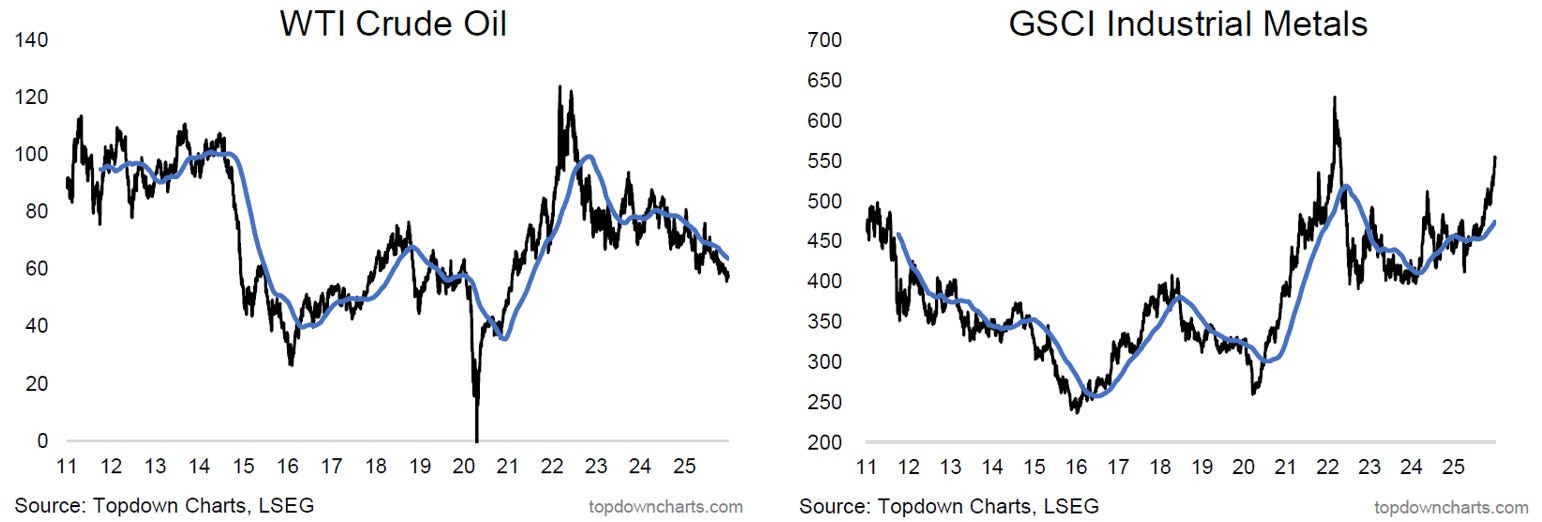

In FX, the dollar remains under pressure (particularly vs Asia/EM and commodity currencies). Meanwhile commodities remain a mixed bag with crude oil under pressure, industrial metals rising, precious metals pulling back from the highs, and agri mixed-to-weaker.

Market themes: Global Equities...

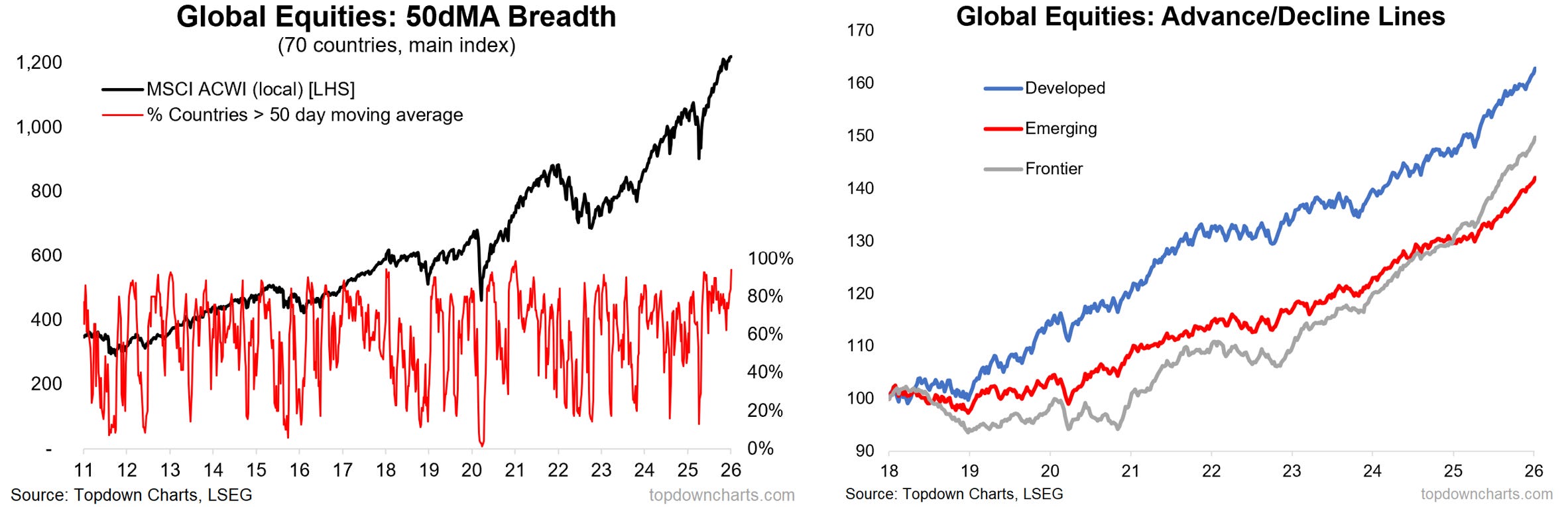

-Global Equities are making a strong start to 2026

--breadth is surging, following the brief minor correction late last year

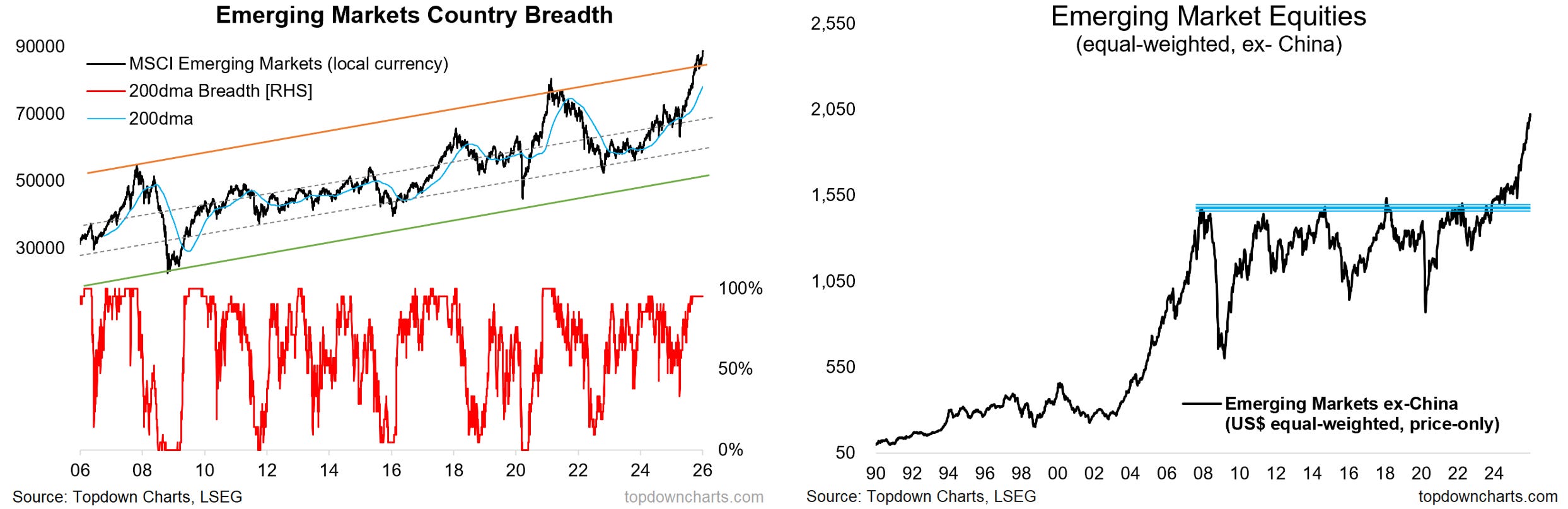

--emerging markets are going strong on all angles

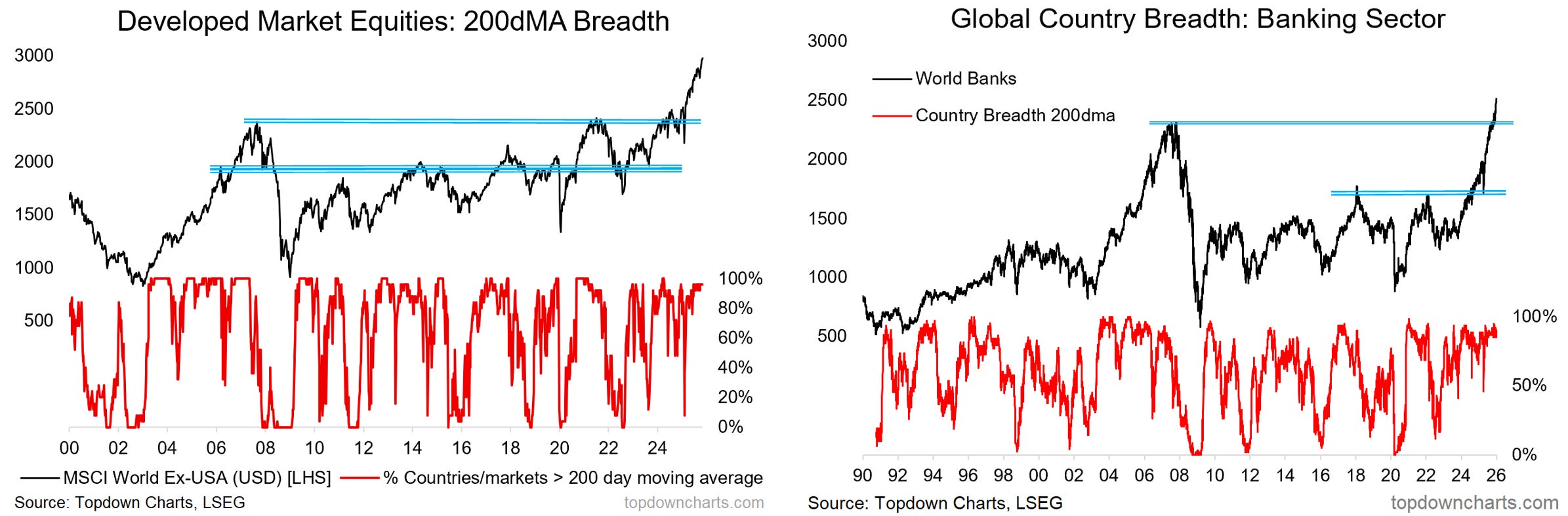

--developed markets are also strong, and global bank stock strength is helping

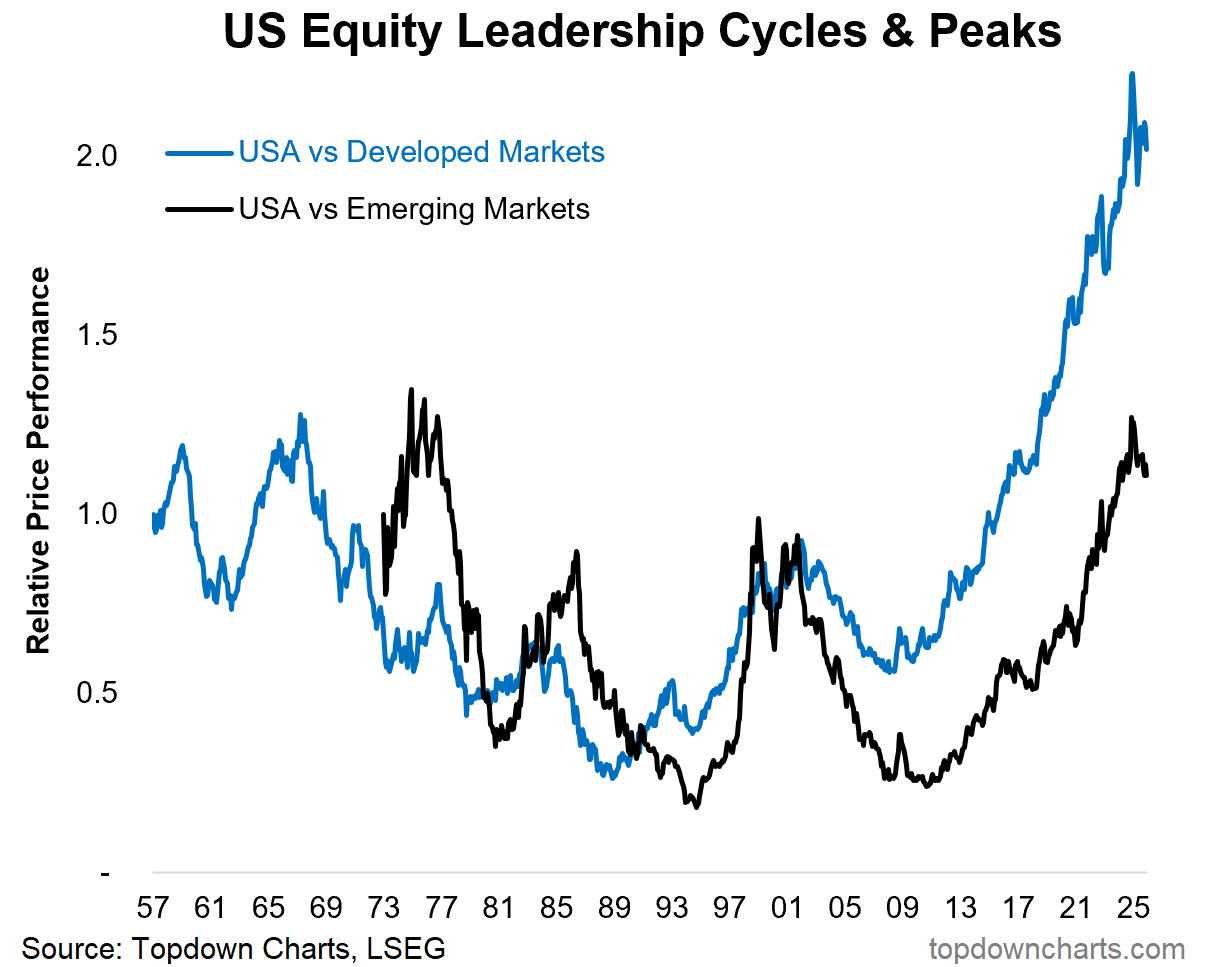

--as a result of global equity strength, we’ve seen a turning point in global vs US equity relative performance.

-Overall it’s a good sign for global equities.

Global Equities are perking up again after a brief minor correction in November last year; short-term breadth is surging after resetting to the bottom end of the post-April range, and country-level advance/decline lines across the 3 major buckets within global equities are moving sharply higher; indicating broad strength across countries.

Emerging Markets have had a particularly strong run over the past year, and this momentum looks to be gracefully carrying over into 2026, with the MSCI local currency EM index pushing higher (with strong breadth, wide participation) and the big breakout in the equal-weighted US$ EM index seeing further follow-through.

But developed markets (ex-US) are also going strong, and have likewise seen upside breakout follow-through following the brief pullback late last year. A key source of strength in global equities has been the surge in global bank stocks; initial breaking out of the 2017-2025 trading range, and then surging on to new all-time highs last year; again all with strong breadth.

The strong run in developed and emerging markets is helping reinforce the global vs US equities theme, and as things currently stand the high point in US outperformance vs global has been and gone -at least for now.

So a key theme to keep track of is going to be whether the turning point in global vs US equities relative performance turns out to be another bump in the road or a true turning point.

Macro & Markets: This week we get the rest of the December PMI data, China CPI/PPI, and US jobs data.

In markets, the US 10yr yield is pushing up against 4.20% resistance, DXY rebounding off lower support levels, gold pulling back to support, WTI crude pressuring support, bitcoin rallying off support, stocks sold-off to short-term support…

Research Agenda: Will be working on the Q1 Quarterly Strategy Pack this week (with particular emphasis on the 2026 Outlook).

And, in case you missed it -- the December monthly pack was sent out last week.

Best regards,

Callum Thomas

Head of Research | Topdown Charts Limited | www.topdowncharts.com

Mobile: (+64) 22 378 1552

Email: callum.thomas@topdowncharts.com