Hello and welcome to a new week - hope you have a good one!

The latest Global Cross Asset Market Monitor [Market Chart Pack] is attached below:

Topdown Charts Global Cross Asset Market Monitor 26012026

Global Markets Monitor -- Notable Developments

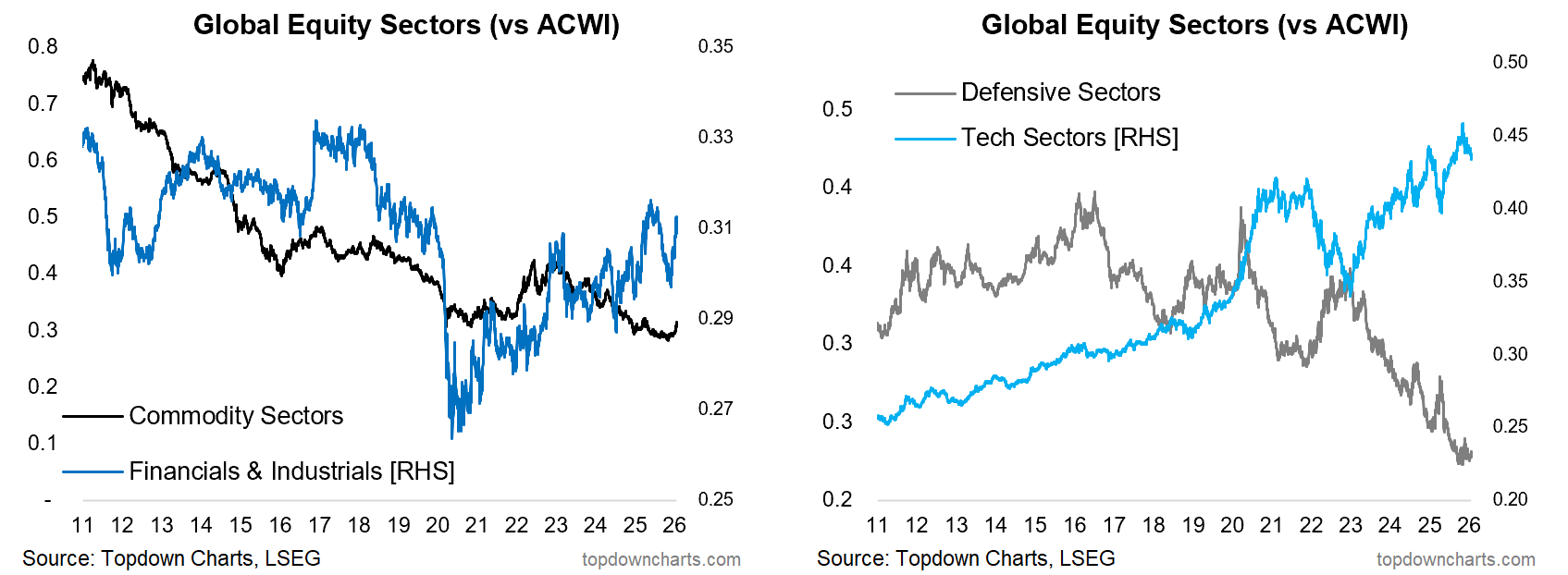

Stocks into a bit of consolidation last week, but still progress on rotation to global vs US. In sectors seeing commodity sectors gaining ground (especially materials; given strength in precious metals + base metals), tech and tech related still lagging, and defensives consolidating.

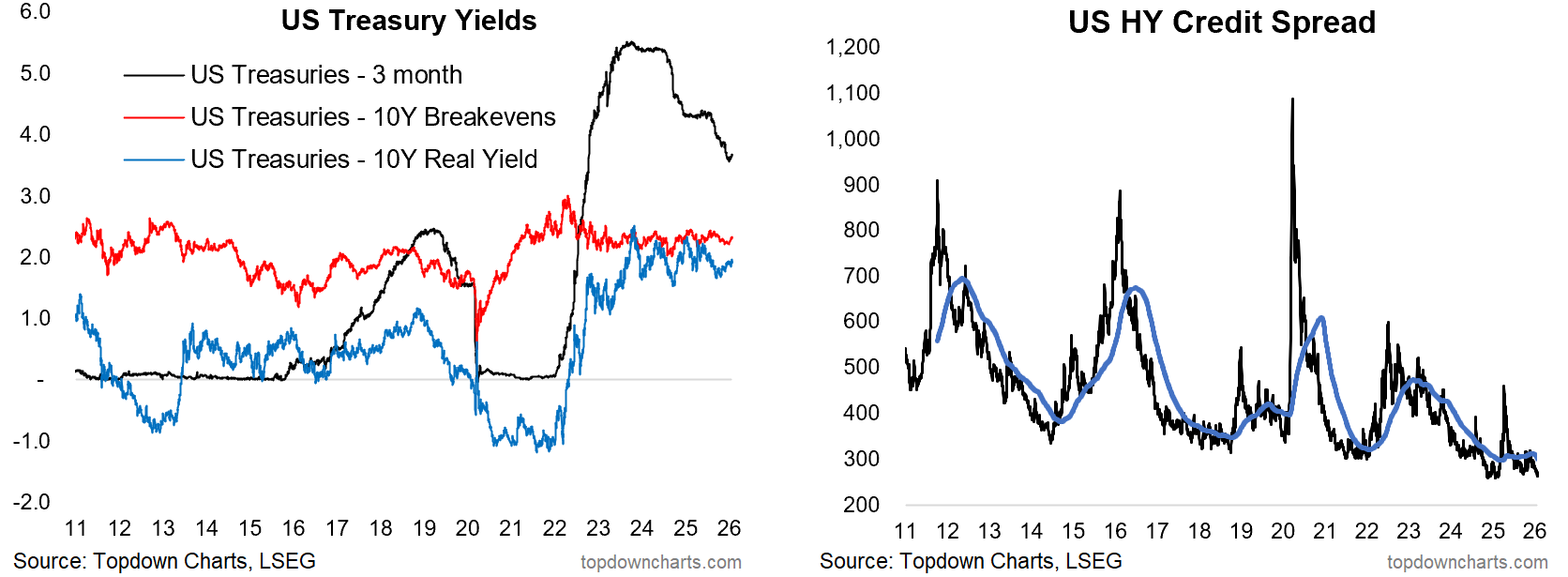

Treasury yields are up off the lows across the curve, but still volatile and no decisive moves as yet. Credit spreads and risk pricing remain calm and confident.

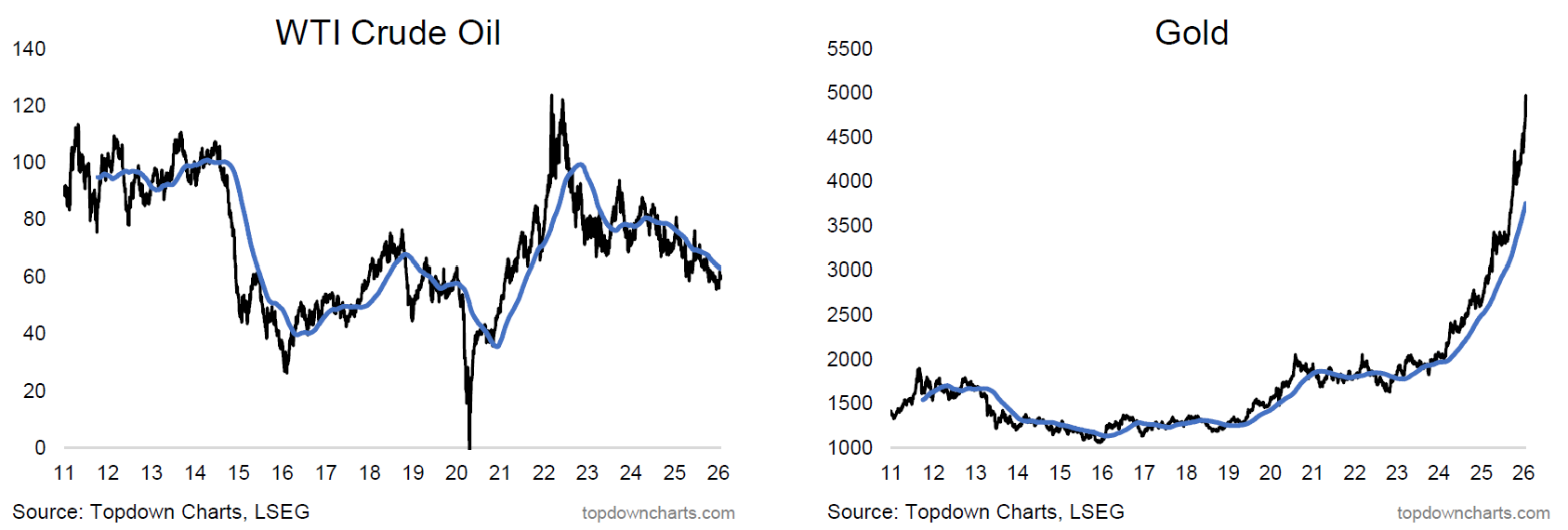

In FX, the US dollar is losing ground on a fairly broad basis. Commodities still mixed, energy up off the lows, precious metals going strong, base metals elevated but consolidating, livestock up, agri down.

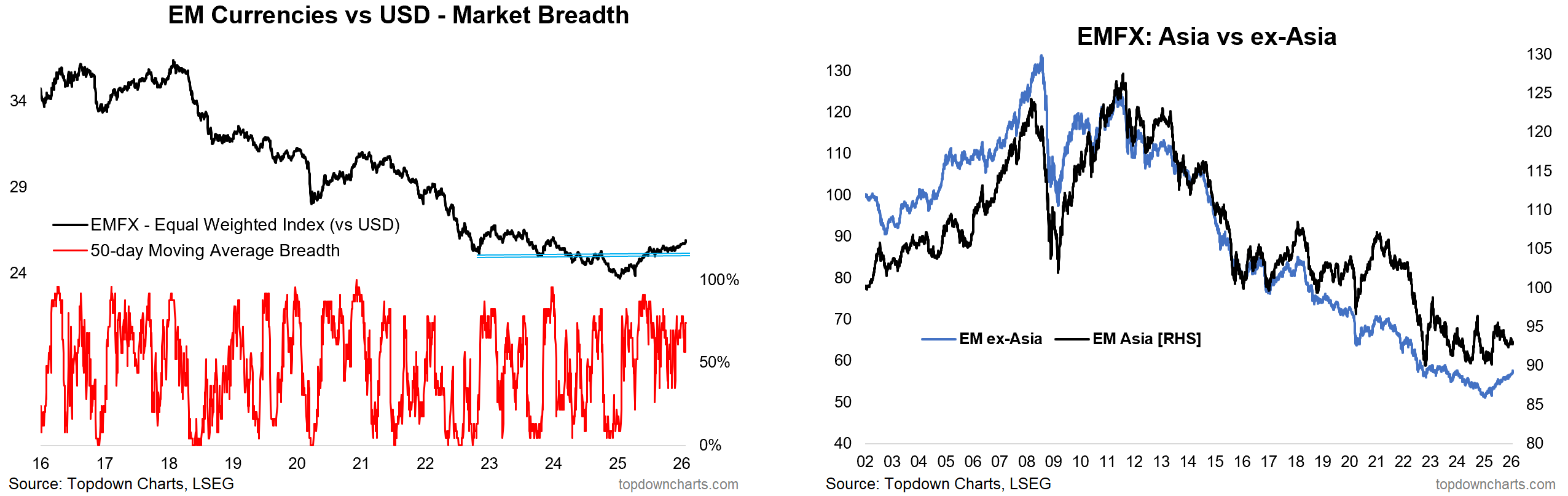

Market themes: Commodities & EMFX

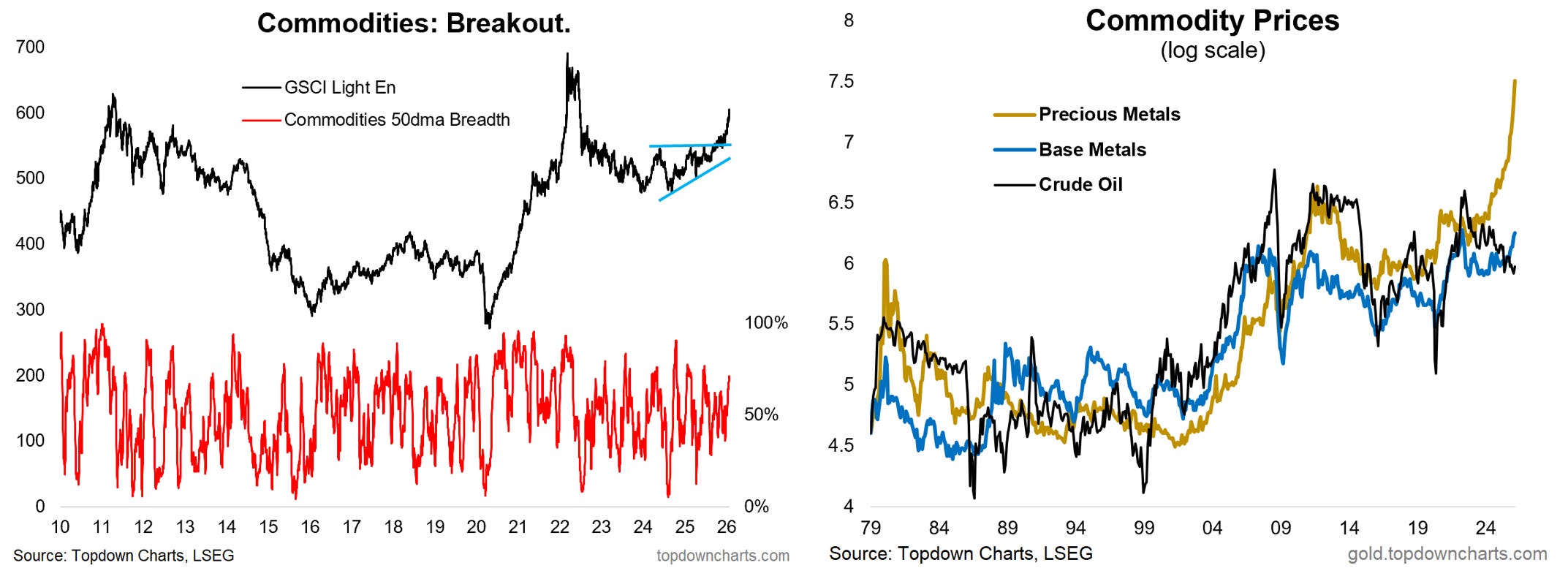

-Commodities are seeing good follow-through in their upside breakout.

-EMFX is also starting to perk up (especially EM ex-Asia).

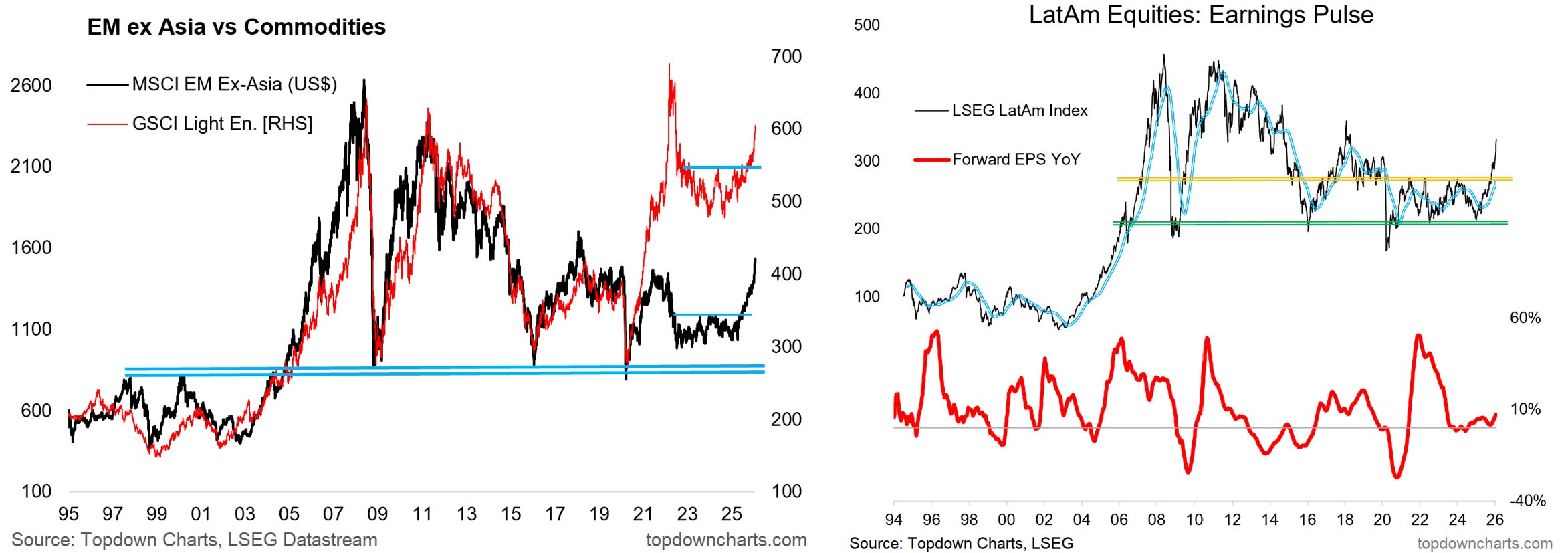

-EM equities ex-Asia and commodities are seeing good cross-confirmation, and overall these are bullish developments for EM and commodities.

Commodities are heating up, the GSCI light energy index is seeing significant follow-through in its breakout. The key driver has been precious metals, but increasingly also base metals. Meanwhile crude oil appears to have found a floor for now with a combination of geopolitics and growth helping offset the oversupply narratives. Overall very bullish technical picture for commodities.

On a similar and somewhat related note, EMFX is also starting to pickup; extending its gains after reversing from its failed breakdown in 2024/25 and following-through on its breakout back above support. Much of the strength is coming through in EM ex-Asia (which in a number of respects is an echo of the renewed strength in commodities we’re seeing).

Indeed, looking at the chart of commodities and EM ex-Asia equities, we can see clear cross-confirmation, and on that note a big part of EM ex-Asia is LatAm; which is likewise undergoing a major breakout (the geopolitical risk window has come, happened, and gone, and likely fades further as attention shifts to Iran).

So overall some promising bullish developments for commodities and emerging markets.

Macro & Markets: This week we get US house prices, consumer confidence, PPI, and interest rate decisions from the Fed and Bank of Canada.

In markets, US 10yr yield and DXY pulling back after initial moves higher, gold pushing higher into 5000, WTI crude pressuring resistance, bitcoin making a run on support, stocks consolidating…

Research Agenda: Will be looking into global equities, risk-on/growth themes.

And, in case you missed it -- the key conclusions from the latest Weekly Macro Themes report (let me know if you did not receive it):

1. Treasuries: Cheap valuations, very low allocations, and consensus bearish sentiment/positioning make for a contrarian bullish setup, but the tactical elements are lacking right now (monitoring the situation).

2. Inflation Risk: The risk of a second wave of inflation is credible, and therefore higher-for-longer risk remains a threat for nominal bonds (but may help TIPS[breakevens]).

3. Stocks vs Bonds: The longer-term/strategic charts are pointing to downside risk for stocks vs bonds, but the tactical elements are opposite (bullish technicals, benign macro).

4. Oil & Energy Stocks: Remain vigilant to upside risk in the oil price, and in particular for energy stocks (which are under-allocated, undervalued, and under-the-radar despite promising technicals).

5. Japan Equities: Remain bullish Japanese equities given the improved macro-fundamental backdrop, scope for upside valuation re-rating, light allocations by global investors, still positive ERP.

Best regards,

Callum Thomas

Head of Research | Topdown Charts Limited | www.topdowncharts.com

Mobile: (+64) 22 378 1552

Email: callum.thomas@topdowncharts.com