Hello and welcome to a new week - hope you have a good one!

The latest Global Cross Asset Market Monitor [Market Chart Pack] is attached below:

Topdown Charts Global Cross Asset Market Monitor 16022026

Global Markets Monitor -- Notable Developments

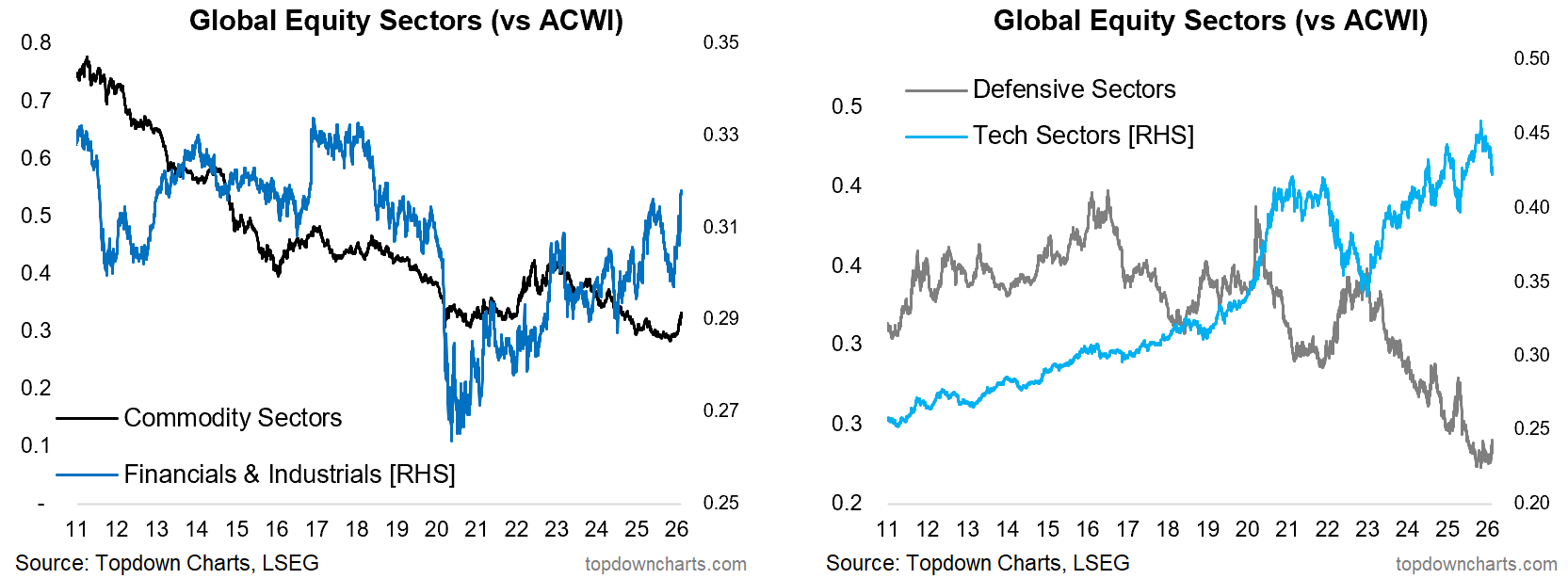

Rotation remains the key word, with strengthening absolute returns in cyclicals/global outperforming vs faltering tech/US. Notably, we are starting to see defensive stir (rather than just tech-to-cyclicals rotation so far; more on this issue further down).

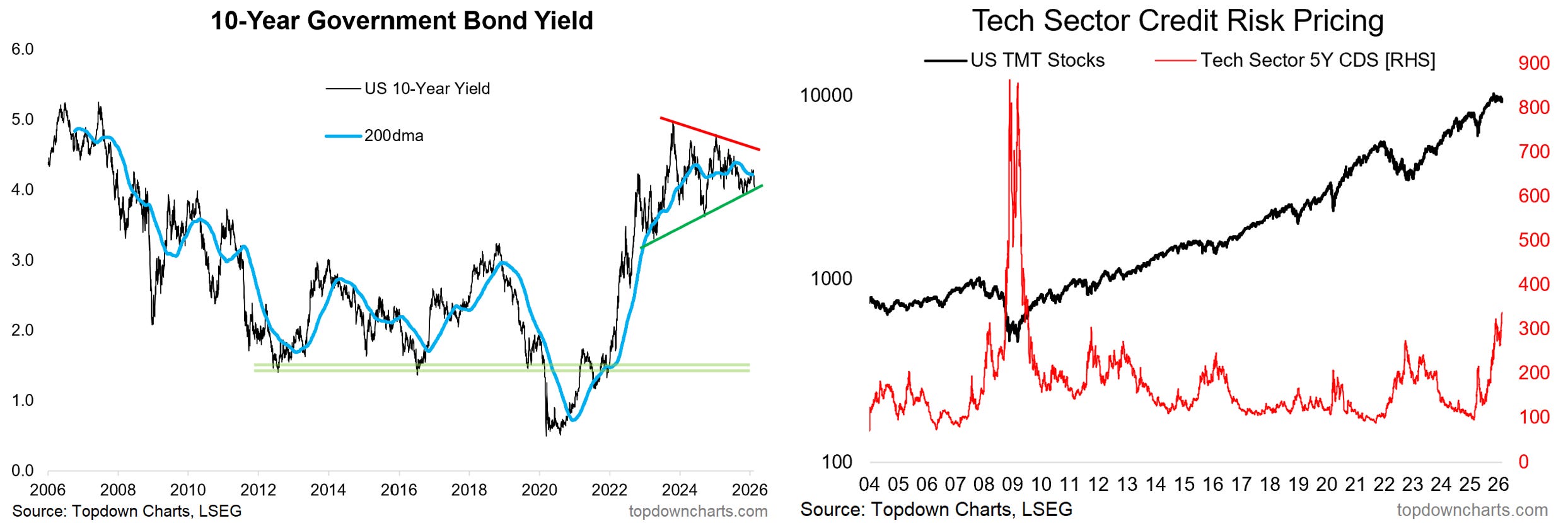

In fixed income, late-week saw US 10yr yields ticking lower after an initial run higher. Also of note in the fixed income space has been new highs in tech sector CDS pricing, as tech stock weakness is spilling over into credit markets (isolated to tech for now).

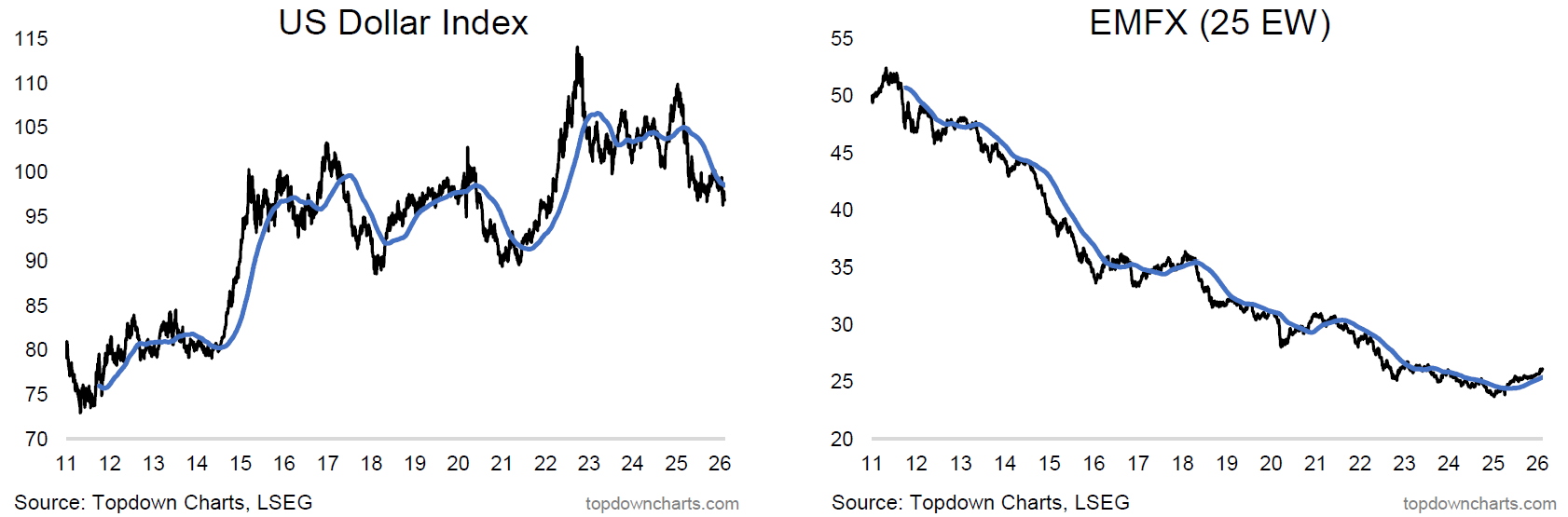

In FX, the USD remains under pressure, Asian/EMFX tending stronger (particularly CNY). Commodities remain a mixed bag yet a common theme is consolidation following previous initial strength (especially in areas of previous recent strength e.g. precious metals).

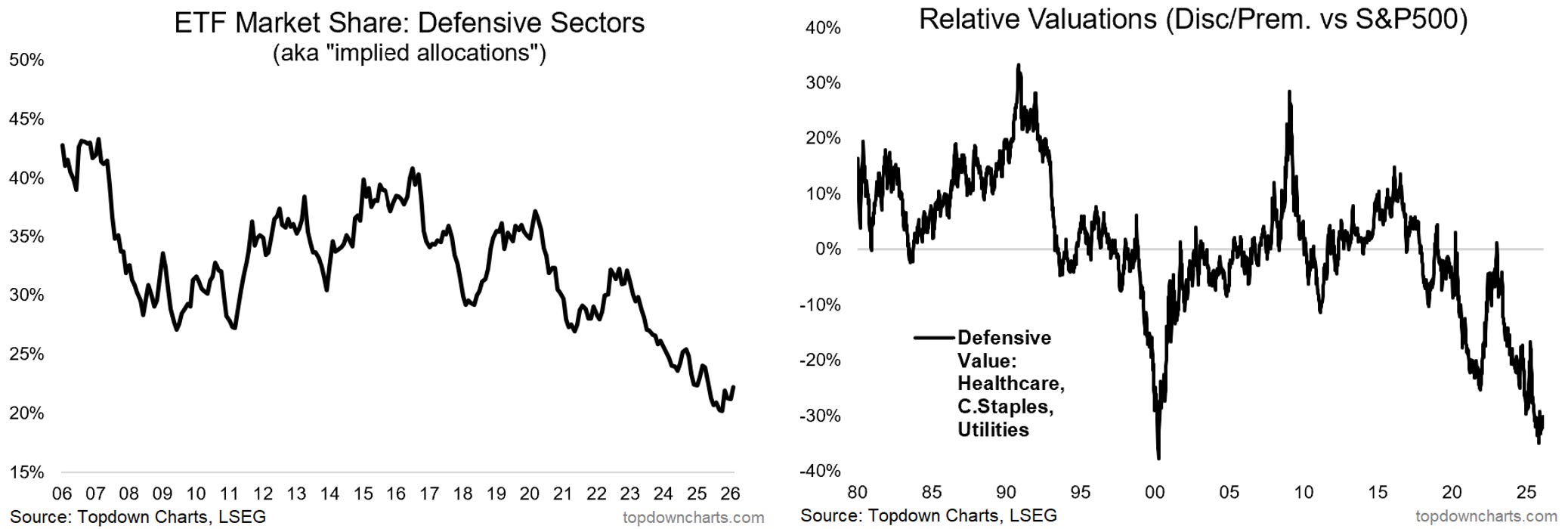

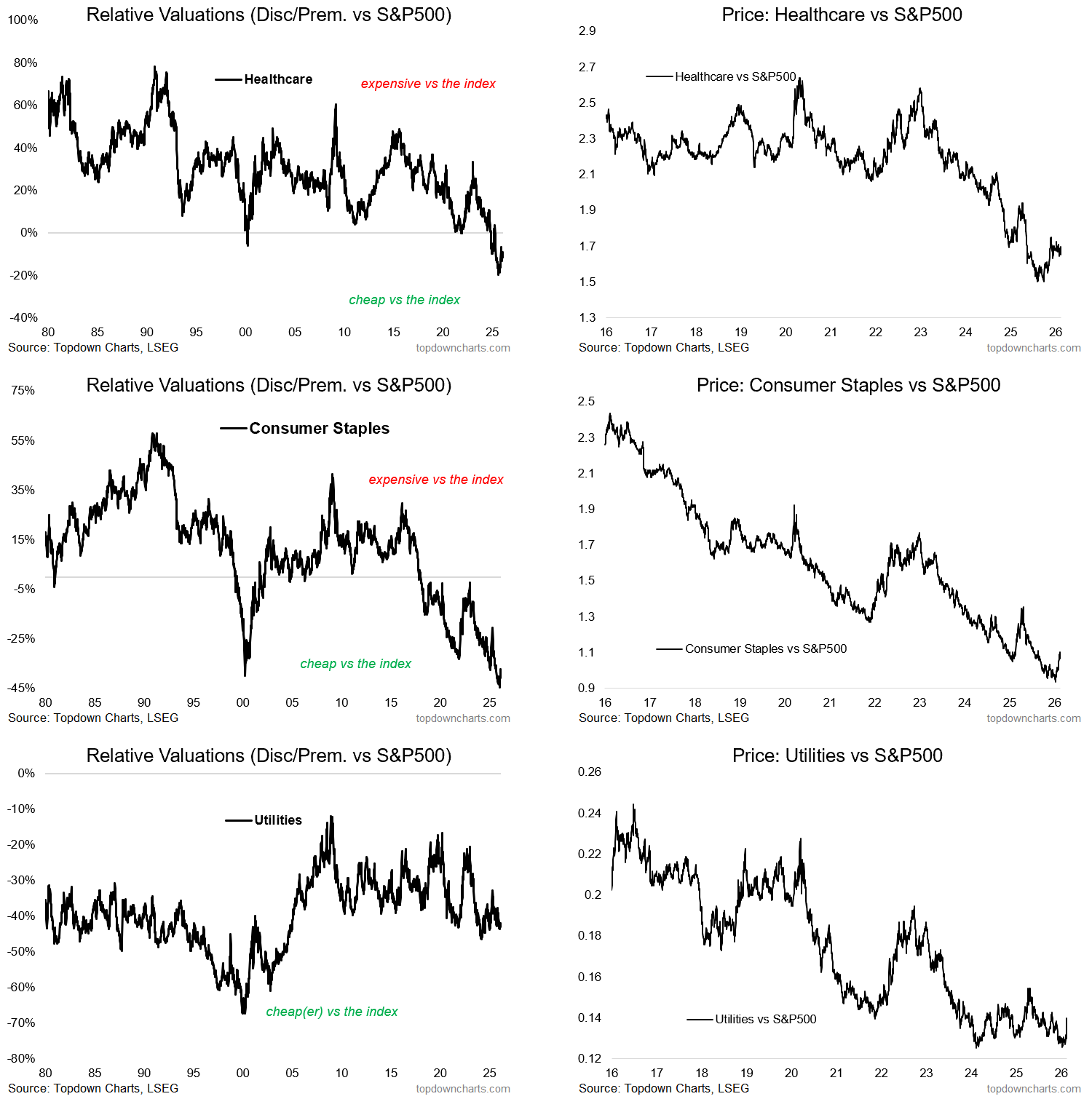

Market themes: Defensives...

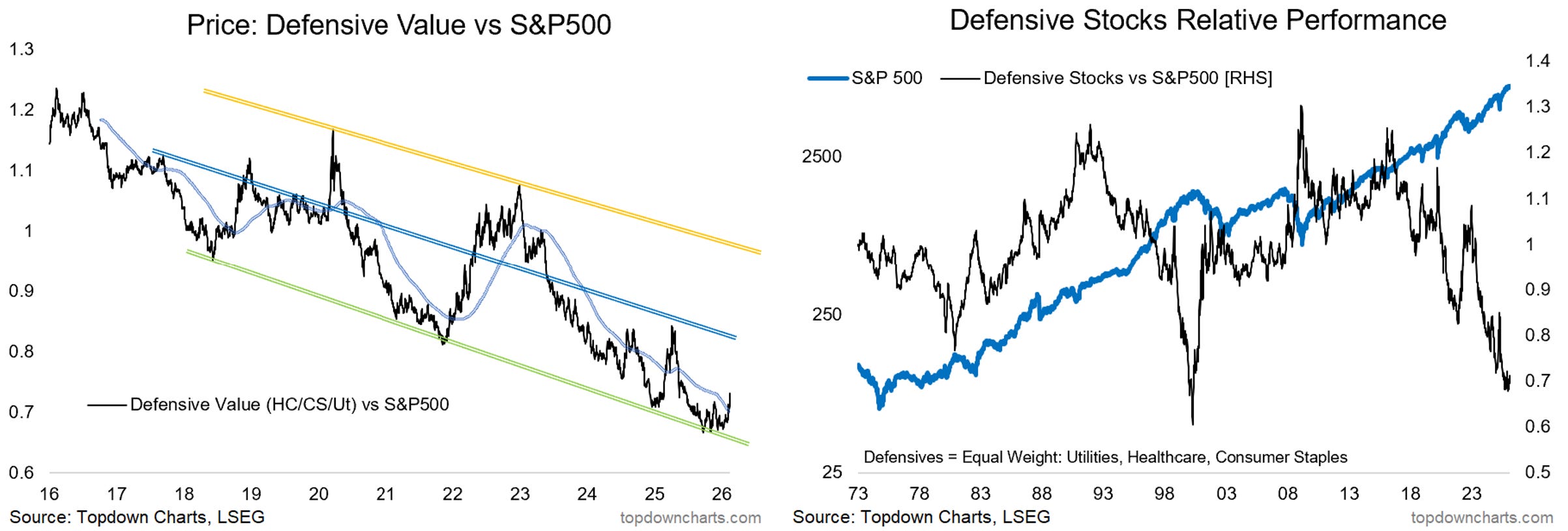

-Defensive stocks made new relative highs late last week.

--this is coming from extreme low allocations and relative valuations.

-Relative strength in defensives is a contrarian bearish risk signal for stocks.

A key development late last week was new relative highs in defensives vs the S&P500, with the equal-weighted basket of defensives breaking out vs its 200-day moving average to multi-month highs (and with bullish relative breadth divergence). This is an important development because defensives were looking stretched to the downside (a contrarian bearish risk signal for stocks), and if this marks the start of a sustained/larger move higher that would be bearish for US stocks (which are already on thin ice with the tech troubles).

As noted, defensives were and are still looking stretched; investor allocations are ticking up from record lows, and the relative value indicator for defensives is ticking up from levels very close to matching those seen at the peak of the dot com bubble. So a promising setup for defensives (in relative terms), and concerning one for the stockmarket as a whole).

Sector-by-sector, consumer staples and utilities have seen the biggest relative gains, but healthcare also looks primed to move higher after a period of consolidation.

Overall there is a consistent picture here.

Macro & Markets: This week we get US NAHB, FOMC minutes, Philly Fed, and Q4 GDP figures. We also get the Feb flash PMIs, and a reminder that China is closed for Chinese New Year this week.

In markets, US 10yr yields are pushing lower, DXY holding support, gold consolidating around 5k, crude oil hovering at short-term support, stocks mixed (S&P500 down to support — but tech down, cyclicals holding up).

Research Agenda: This week I’ll be digging into fixed income and FX, but also of course keeping tabs on tech.

And, in case you missed it -- the key conclusions from the latest Weekly Macro Themes report (let me know if you did not receive it):

1. US Tech Stocks – Risk-Watch: US tech stocks have seen a significant deterioration in technicals following the peak back in October 2025, there is material risk of larger downside for tech stocks (and risk to US stocks in general) given expensive starting point valuations and excesses in sentiment/positioning.

Best regards,

Callum Thomas

Head of Research | Topdown Charts Limited | www.topdowncharts.com

Mobile: (+64) 22 378 1552

Email: callum.thomas@topdowncharts.com