Hello and welcome to a new week - hope you have a good one!

The latest Global Cross Asset Market Monitor [Market Chart Pack] is attached below:

Topdown Charts Global Cross Asset Market Monitor 23022026

Global Markets Monitor -- Notable Developments

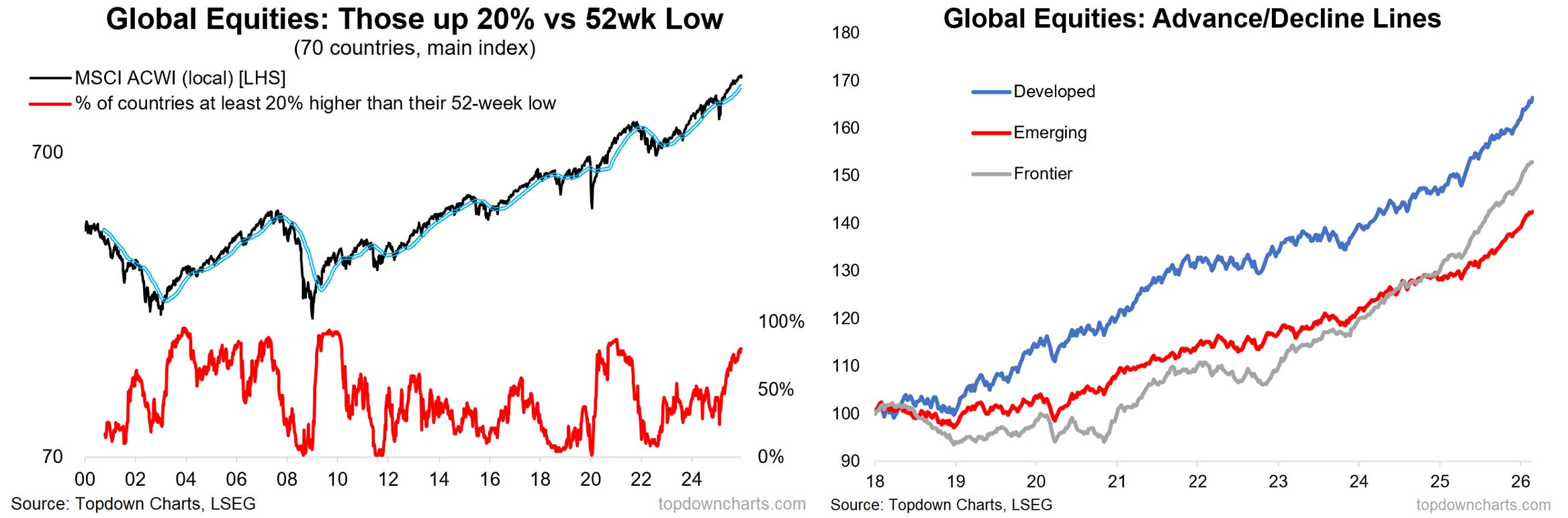

Stocks remain a bit of a mixed bag, with US consolidating (tech down, ex-tech up), and global continuing to advance (global equity bull market very much alive and well by all accounts + rotation remains in play).

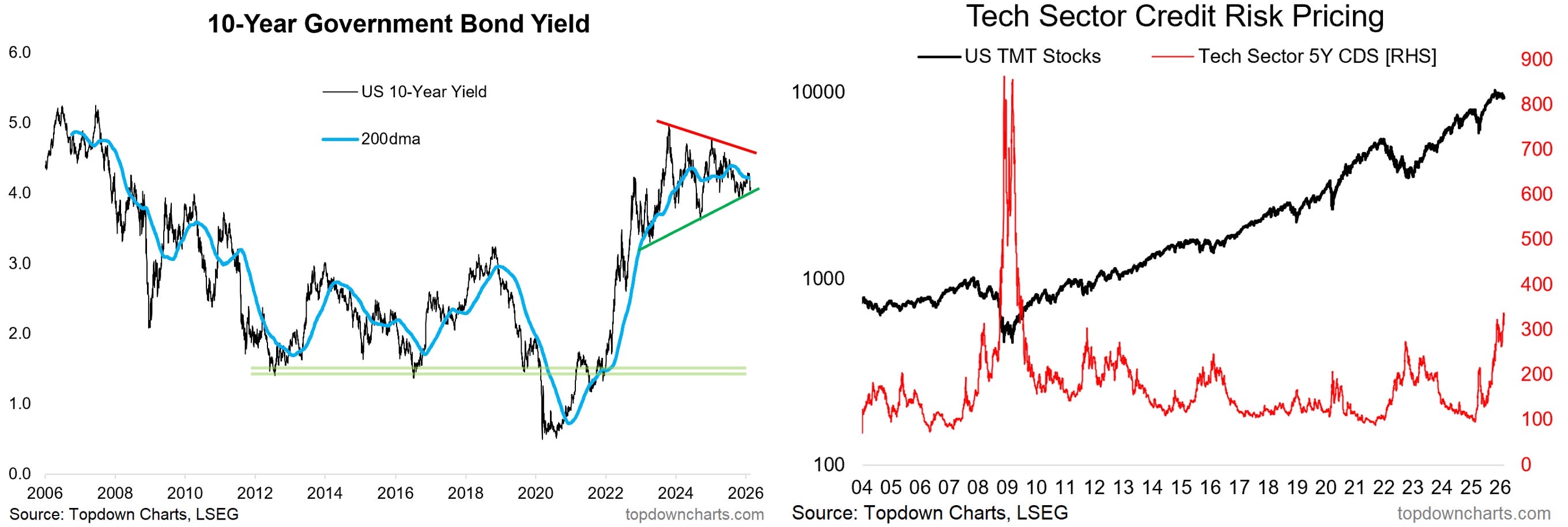

In fixed income, treasury yields continue to see downward pressure, but still confined within the range (awaiting catalyst one way or the other i.e. growth scare/risk-off vs inflation/reacceleration). Credit spreads have ticked up off the lows, but the main point of interest in credit markets has been the continued uptrend in tech sector CDS pricing (and emerging downtrend in tech stock prices).

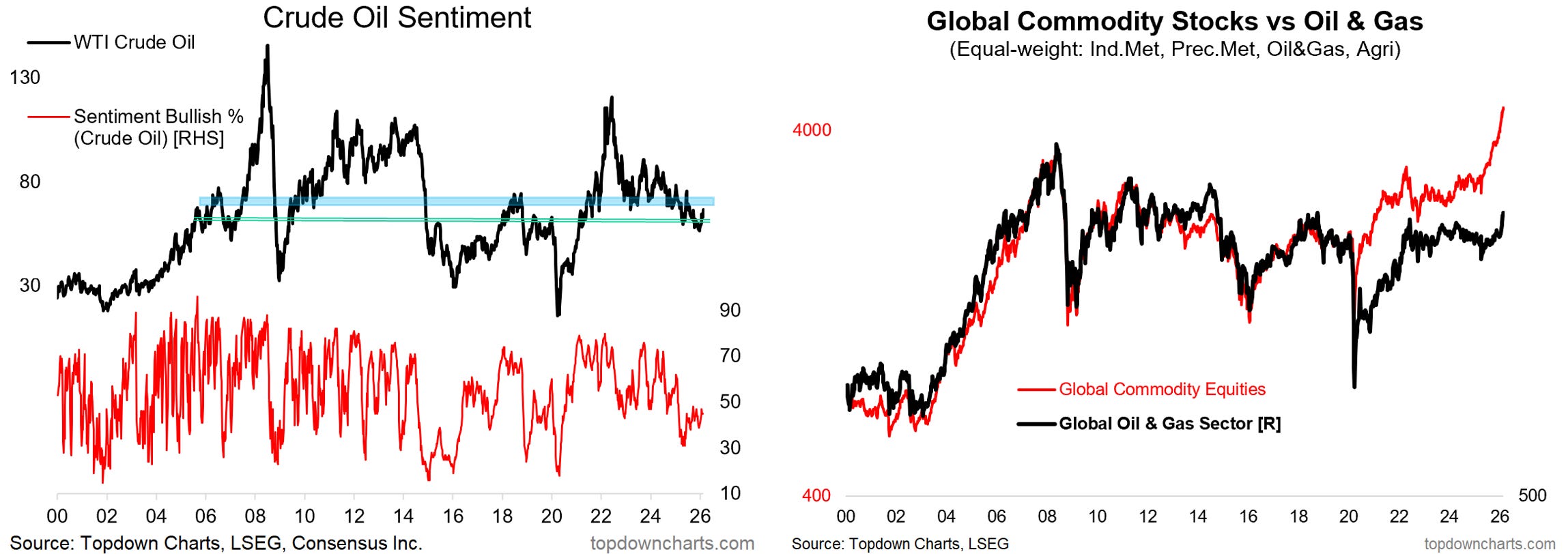

In FX, it’s a picture of consolidation and stalemate. Commodities continued to see mixed prospects, but this time with energy prices picking up vs industrial metal prices coming off the boil, and precious metals still volatile, and agri soft. The Iran situation continues to develop, with ostensible progress/posturing on negotiations for a deal, but otherwise a steady and substantial build-up of US strike + defense capabilities in the region; which is helping energy prices tend to the bullish side (and energy stocks starting to catch-up vs the rest of commodity stocks).

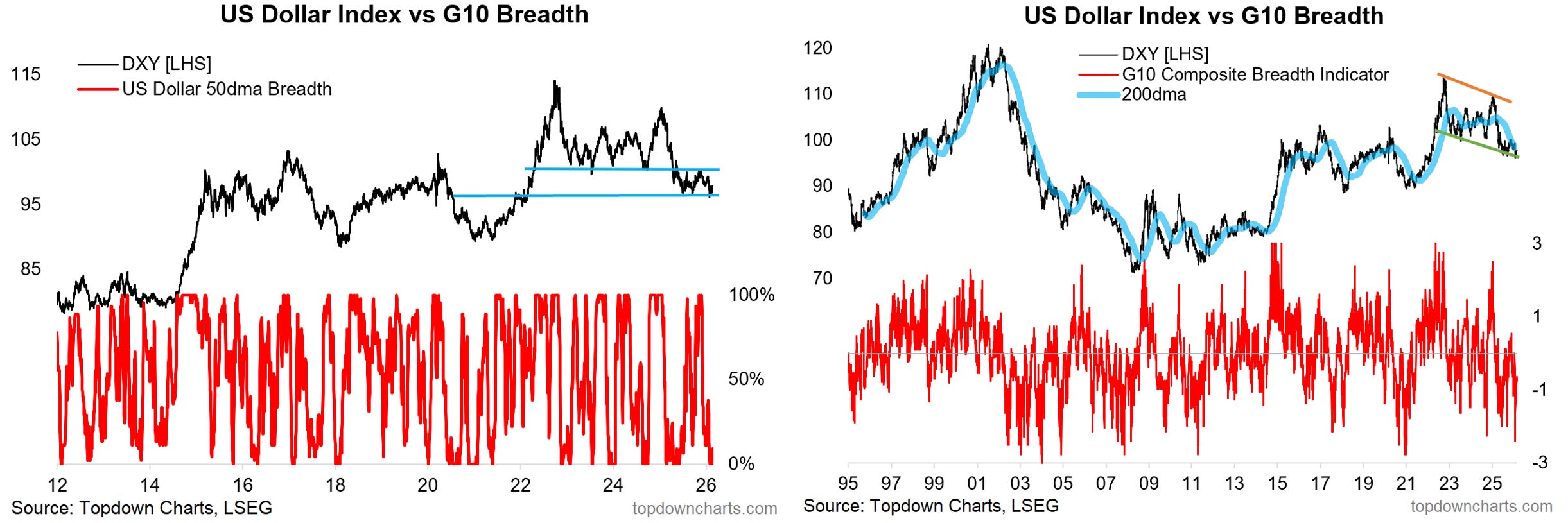

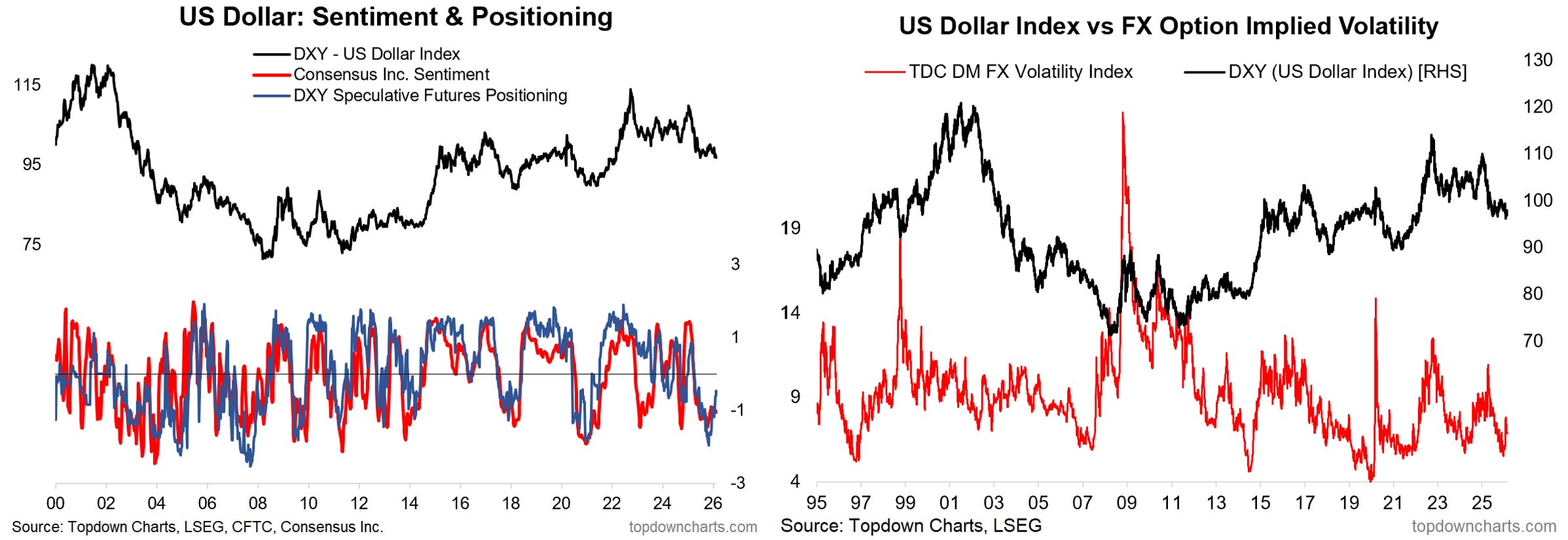

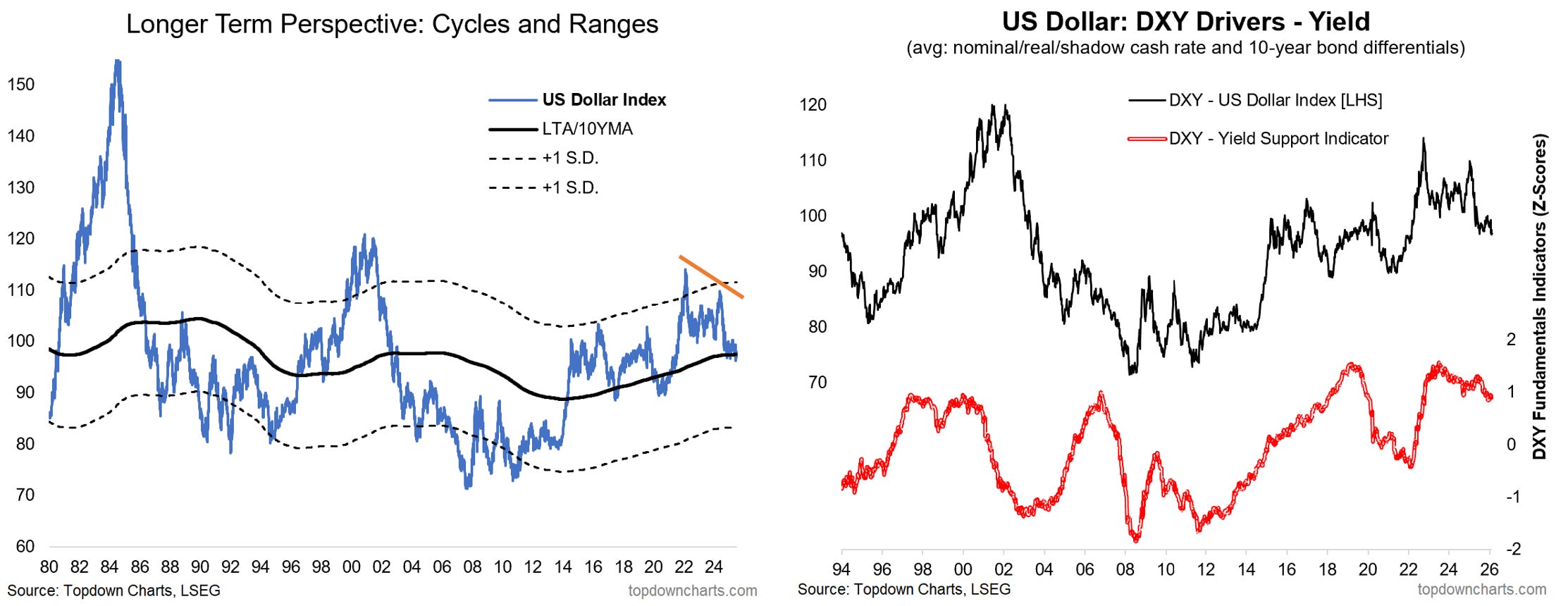

Market themes: US Dollar Outlook...

-DXY is ticking up off support (and oversold conditions)

-Technicals point to risk of a short-term rally

-Yet the bigger/longer-term picture still looks bearish as a larger downtrend looks to be developing (consistent with some of the other macro/market developments).

The DXY has been ticking up off short-term support (and the lower end of its downtrend channel), and with breadth reaching oversold levels. Technically it looks primed for a short-term rally even if the overarching trend still looks to be downwards.

Meanwhile sentiment and positioning have been turning up from previously consensus bearish and crowded shorts, and FX market implied volatility has similarly turned up following a crunch to multi-year lows (we often see contractions and surges in volatility around turning points -- either prior to a change in trend e.g. upwards in this case, or a trend acceleration e.g. a breakdown in this case). Given the developing short-term bullish technicals it warrants close monitoring for possible USD strength flare-ups (which would hurt many of the consensus trades like commodities and global/EM equities).

Yet the bigger picture is still skewed to the bearish side, it still has the look and feel of a bearmarket/downtrend developing, valuations are still slightly expensive, and yield support indicators are still tapering downwards.

So I would continue with the overall medium/longer-term bearish bias, but meanwhile mindful of the short-term upside risks.

Macro & Markets: This week we get US house prices, consumer confidence, PPI, and mid-week Trump is scheduled to deliver his State of the Union address.

In markets, US 10yr yield hovering at support, DXY attempting to rally, gold attempting breakout from consolidation, WTI crude pressuring resistance, bitcoin breaking lower, stocks mixed…

Research Agenda: This week I’ll be reviewing fixed income, commodities, equities.

(n.b. there was no Weekly Macro Themes last week as I was moving and did not have time to complete the report, this week will proceed as normal)

Best regards,

Callum Thomas

Head of Research | Topdown Charts Limited | www.topdowncharts.com

Mobile: (+64) 22 378 1552

Email: callum.thomas@topdowncharts.com